ALLPCB

ALLPCB

New technologies and product releases are driving the medical wearable market.

How do medical wearables make patients healthier?

Market context

According to Mems Consulting, most growth in today's wearables market comes from consumer sports, fitness, and wellness. However, wearables are rapidly expanding into healthcare, with the market expected to reach $32 billion by 2024. The proliferation of smartphones, miniaturization of sensors, and ease of integration have significantly increased the number and variety of wearables, and some products have reached performance levels suitable for medical use. But how do medical wearables make patients healthier, and why is this happening now?

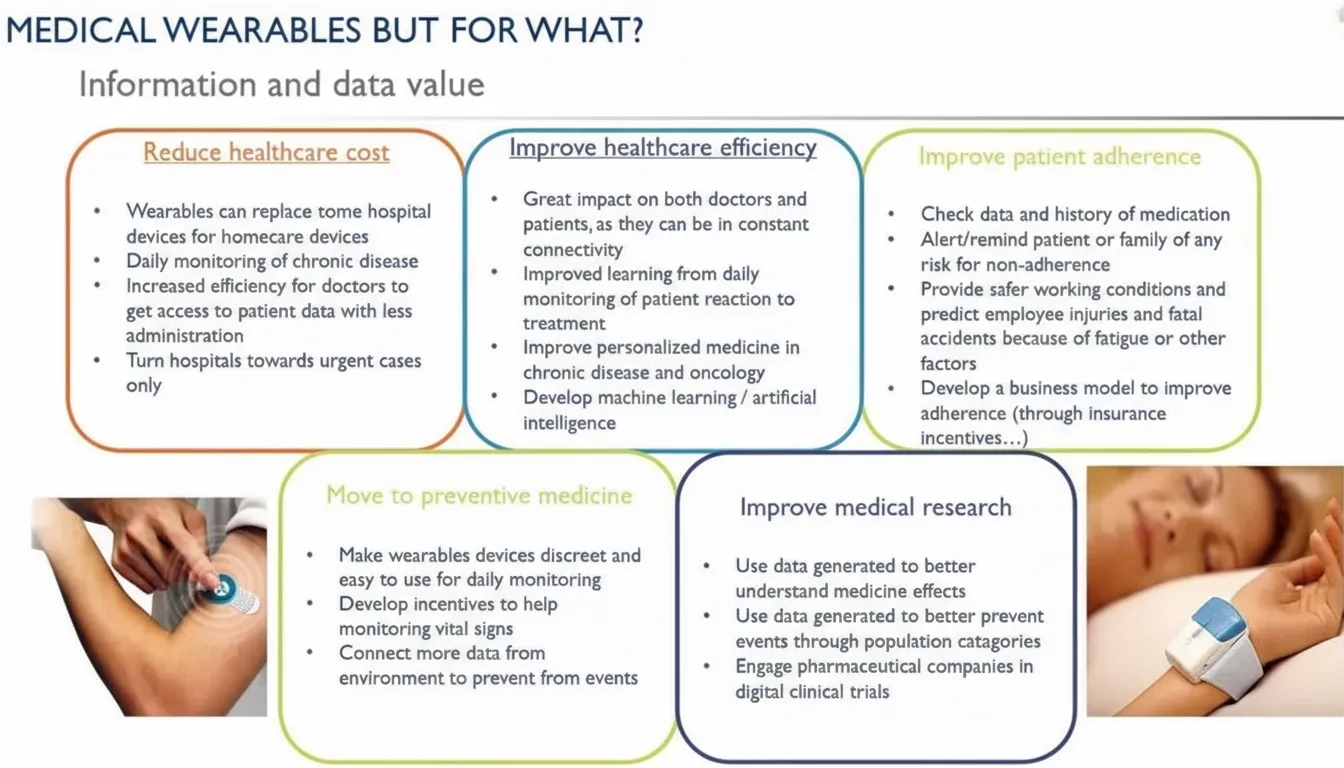

Value of medical wearables

Medical wearables are intended to monitor patients' vital signs to prevent health deterioration and to support disease management and rehabilitation. Manufacturers face medical-industry challenges such as multiple certifications (CE and FDA). With the rising prevalence of chronic conditions such as cardiovascular disease and diabetes (around 425 million people worldwide with diabetes), the demand for health monitoring is increasing, and the advantages of medical wearables outweigh regulatory hurdles. More wearables are reaching medical-grade performance, including products such as the Ava bracelet, Apple Watch, Cefaly headband, Ectosens patches, Omron smartwatches, and Verily smartwatches. Functions range from activity tracking to sleep monitoring and glucose sensing. As consumer medical wearables, these devices have potential, but they must meet accuracy, comfort, and usability requirements. Apple Watch Series 4 received FDA clearance for its ECG and heart monitoring features, indicating greater openness from regulators toward these technologies. Questions remain about how health data from wearables will be handled and who will use it and for what purposes.

New products and ecosystem growth

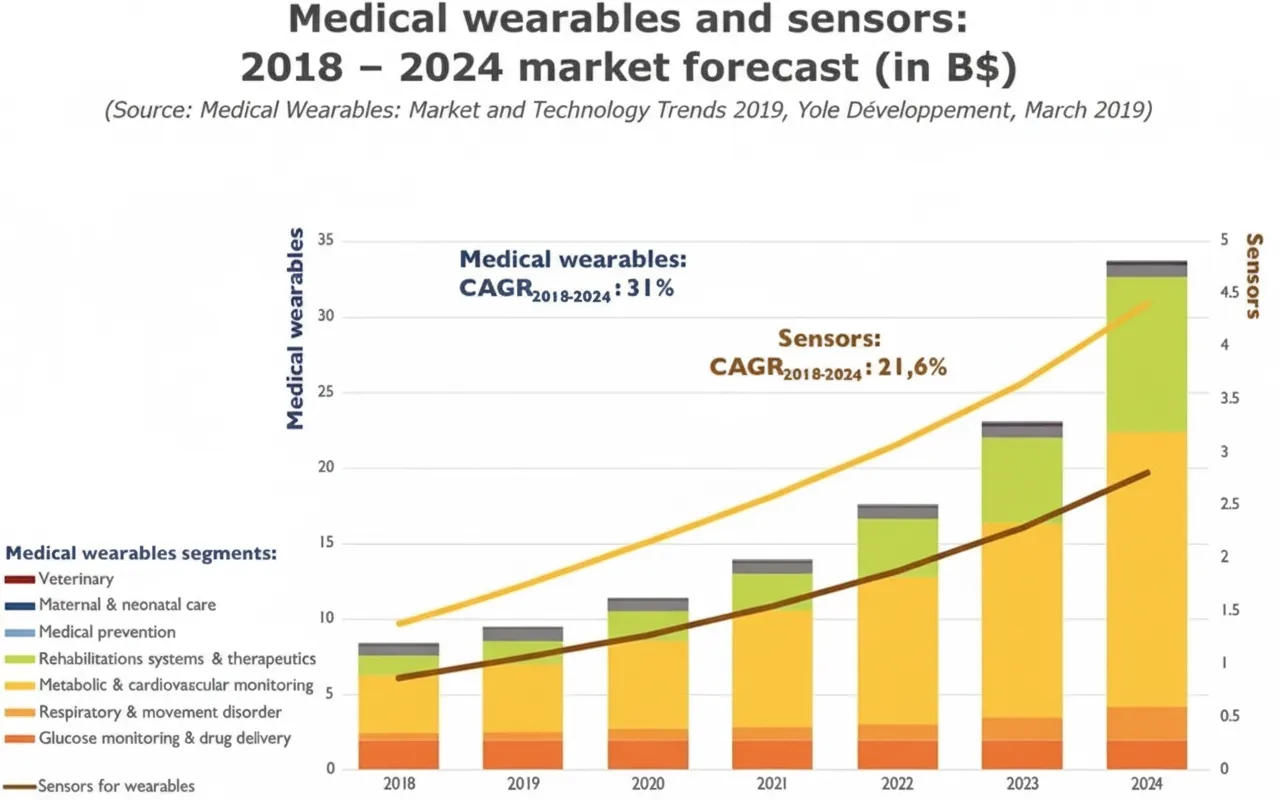

The medical wearable and sensor ecosystem is growing rapidly. The global medical wearable market is expected to grow year?on?year by 31%, reaching $32 billion by 2024. Meanwhile, the global sensor market within medical wearables, including continuous glucose monitoring (CGM), is forecast to reach $2.8 billion by 2024, with a 2018–2024 compound annual growth rate (CAGR) of 21.6%.

Following Apple's Series 4, attention has increased on ECG features in smartwatches, which can provide clinicians with accurate information on cardiac status. At the sensor level, increasing device complexity is pushing electronics companies to become specialists in medical-grade sensors, including suppliers such as ams, Maxim, and Valencell. These suppliers optimize and integrate sensors for area and power while maintaining measurement accuracy.

Since 2014, researchers have tracked more than $550 million raised by medical device and diagnostics companies, and commercialization of novel medical wearables is accelerating. Ongoing investments and acquisitions between large diagnostics companies and consumer firms—such as Apple’s acquisition of the personal health record startup Glimpse, and Medtronic’s acquisition of Nutrino Health—support positive market dynamics.

Pharmaceutical companies are also engaging with medical wearables through strategic partnerships to improve R&D. For example, Pfizer, UCB Pharma, Apple, Johnson & Johnson, and IBM have collaborated on remote monitoring solutions for Parkinson's disease to transform clinical care. Smartwatches and wristbands can provide health information that users may share with insurers and clinicians to inform treatment.

This report provides market data and forecasts for medical wearables and highlights emerging wearable business models.

Technical challenges and advances

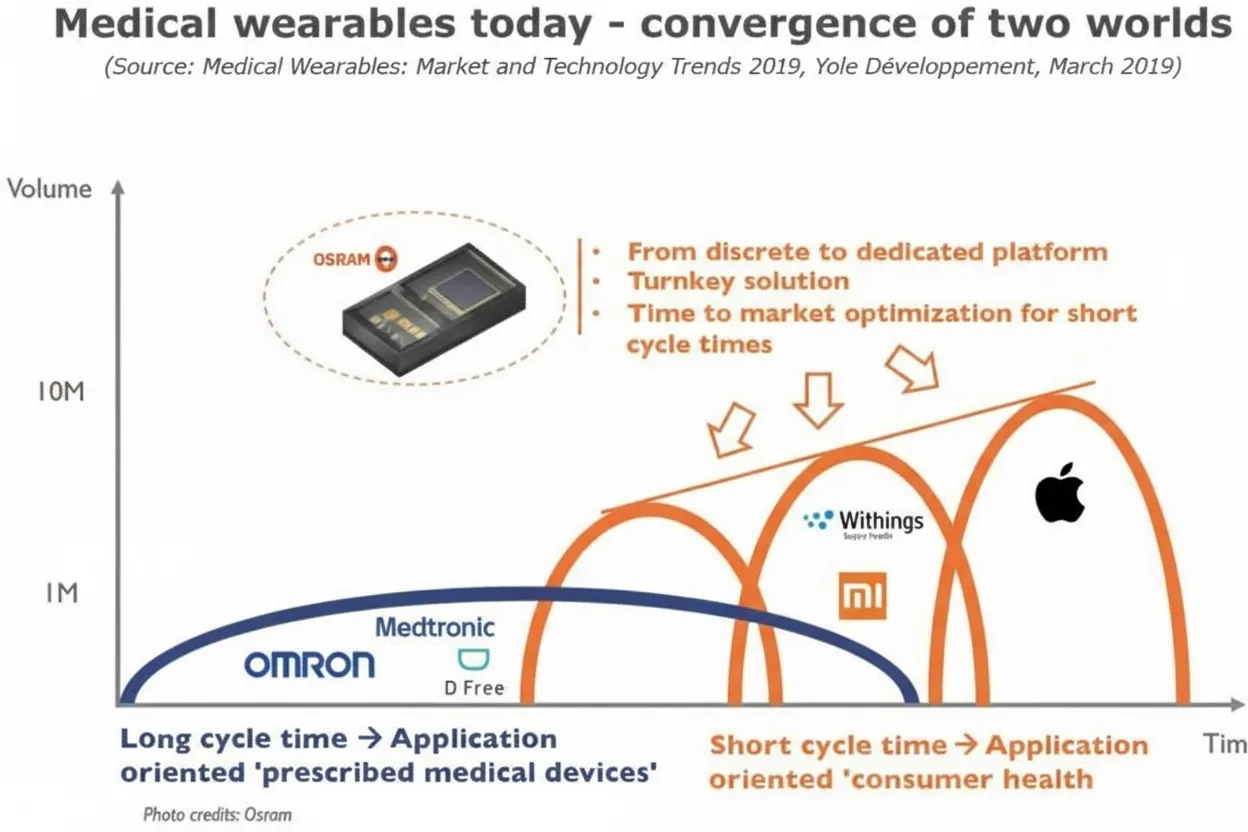

Medical wearables represent a convergence of medical-grade devices and consumer wearables. Participants fall into two broad groups: medical-grade device manufacturers moving into consumer health services, and consumer wearable companies entering higher-value medical markets. As competition intensifies, manufacturers must ensure that collected data meet medical-grade quality and accuracy requirements.

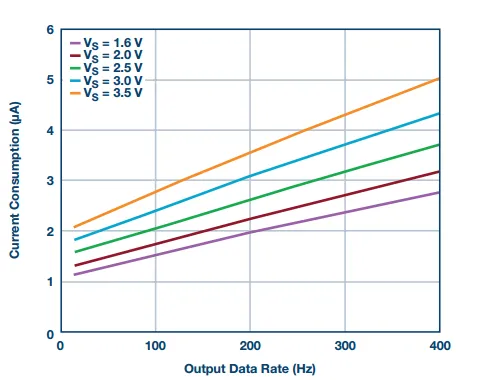

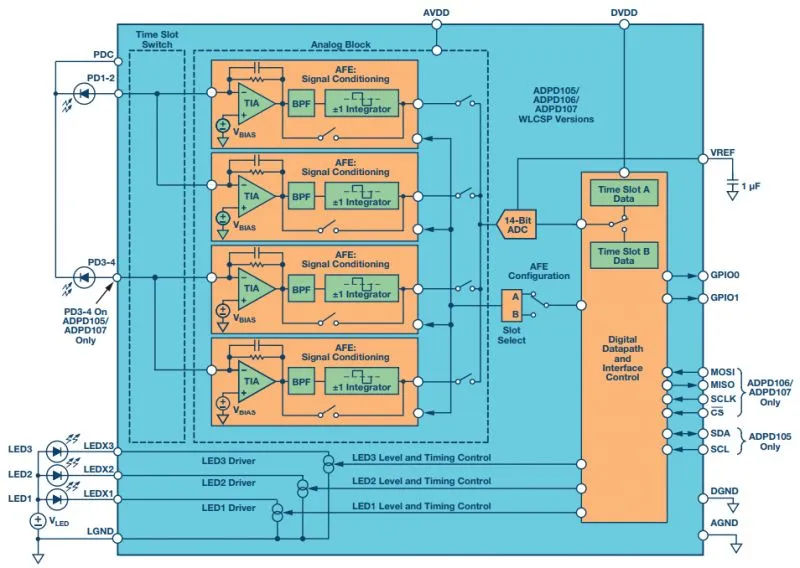

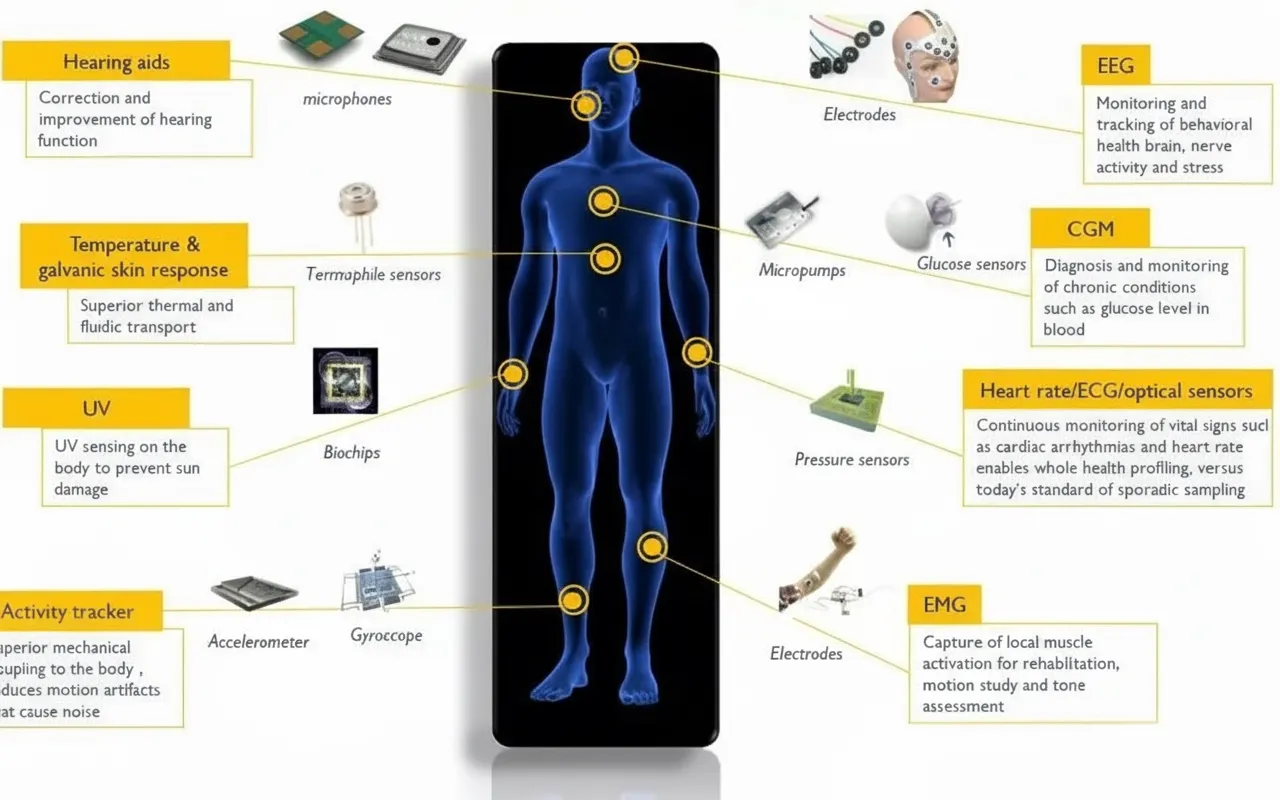

Sensors and electronics manufacturers accelerate time to market using integrable, optimized modules. For example, photoplethysmography (PPG) devices for heart-rate detection integrate LEDs and photodiodes. The PPG signal is the variation in light intensity after reflection from skin and reflects changes in vascular volume, providing physiological information such as heart rate and blood oxygenation. The technique uses LEDs to emit light at specific wavelengths; as blood flow changes with each heartbeat, photodiodes receive periodic pulses corresponding to arterial volume changes, allowing cardiac pulse capture. Sensor designers are developing monitoring modules that package LEDs and photodiodes together to meet miniaturization and low-power requirements while ensuring measurement accuracy. These turnkey solutions help wearable manufacturers shorten time to market and allow sensor suppliers to move upstream in the value chain with higher-value offerings.

High integration and low power are not the only challenges. The report also examines key supporting technologies for medical wearables, such as printed electronics and comfortable flexible materials, which support high-quality measurements and help reduce motion-induced measurement errors.

This analysis of technology trends and roadmaps helps readers understand how the medical wearable industry and its participants address patient and user needs while working to lower overall healthcare costs.