ALLPCB

ALLPCB

Introduction to antenna materials

Antenna materials overview

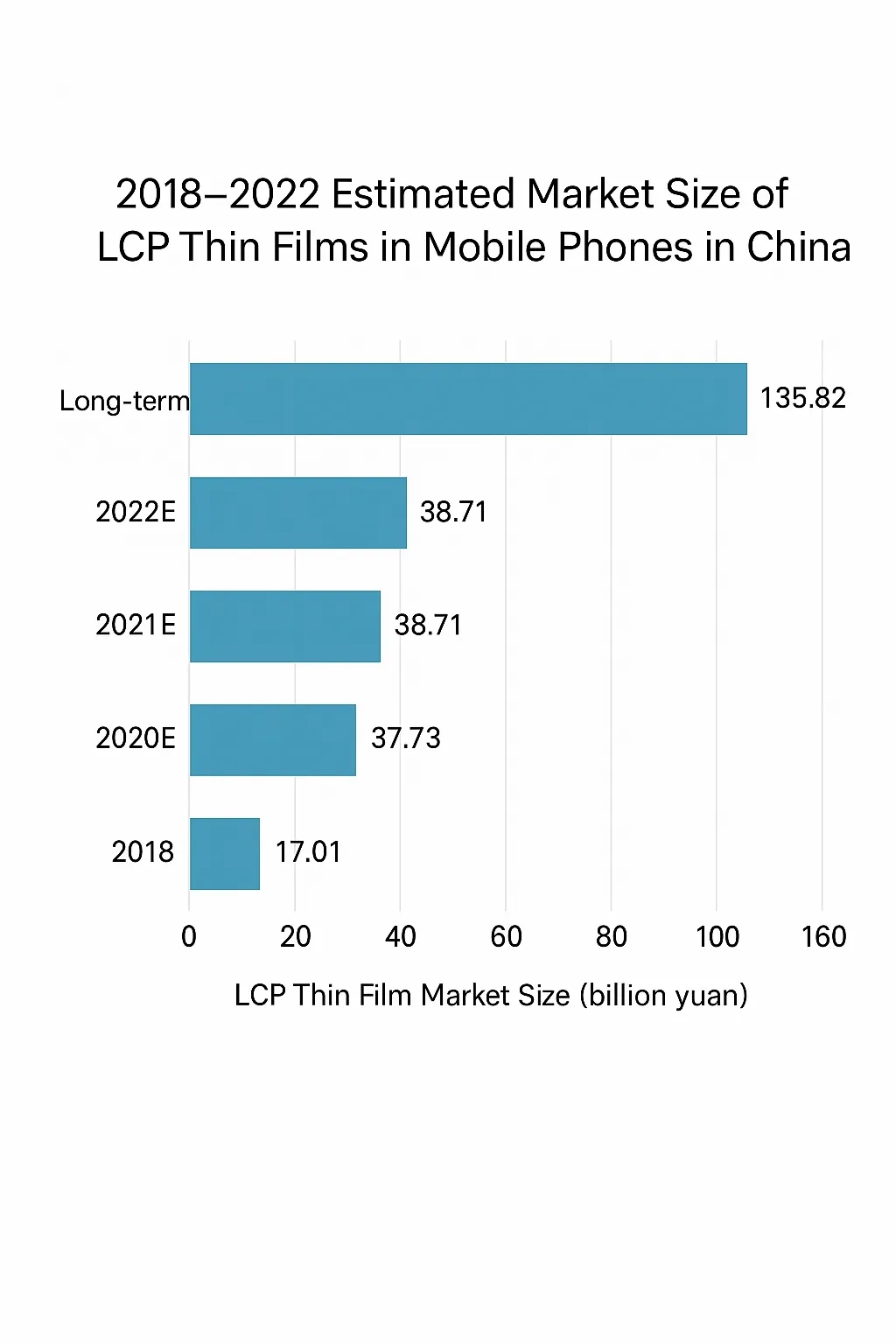

After LCP antennas were introduced in the iPhone, LCP antennas in LCP flexible circuit boards began to grow. Beyond smartphones, LCP antennas will be applied to various smart devices and could be a new growth area for FPC. Demand is expected to expand in camera flex circuits, high-speed transmission lines for laptops, smartwatch antennas, and other applications.

1. 5G antenna materials overview

2013 marked the start of the 4G era. With commercial 5G licenses issued in 2019, 5G deployment has accelerated. In an increasingly automated and connected world, 5G development continues. Estimates show large infrastructure investment driven by 5G; IHS predicts 5G could enable up to $12.3 trillion in global economic activity by 2035 across multiple sectors.

5G refers to fifth-generation mobile communication technology and uses higher radio frequencies. China’s initial mid-band allocations were around 3.3–3.6 GHz and 4.8–5 GHz, with higher bands such as 24.75–27.5 GHz and 37–42.5 GHz under development. International trials commonly use 28 GHz. This pushes 5G toward the millimeter-wave range, whose advantage is high data rates while the primary drawbacks are low penetration and high attenuation. Note: millimeter wave usually refers to 30–300 GHz (wavelengths from 1 to 10 mm), overlapping microwave and far-infrared bands.

2. 5G advantages

Very high data rates: 5G throughput can be orders of magnitude greater than 4G. Users can download a high-definition movie in under a second.

Very low latency: 4G latency is around 140 ms, while 5G can reduce latency to about 1 ms.

High attenuation: Because 5G operates at higher frequencies, signals are more easily blocked, disturbed, and attenuated in transmission media.

3. Material requirements for 5G

Higher transmission speed requires transmission media with low dielectric constant and low dielectric loss.

Limited electromagnetic wave coverage requires materials with strong electromagnetic shielding where needed.

Because 5G signals attenuate more readily, materials with low dielectric constant and effective shielding are desirable.

Components tend to be thinner and must maintain sealing and thermal dissipation, so higher thermal conductivity is preferred.

In summary, 5G needs polymer materials with low dielectric constant, high thermal conductivity, and good electromagnetic shielding properties.

5G antenna material categories

Materials used in 5G communications are diverse: metals, ceramics, engineering plastics, glass, composites, and functional materials all have large market potential. 5G deployment drives the entire supply chain and pressures suppliers to adapt to new technical requirements.

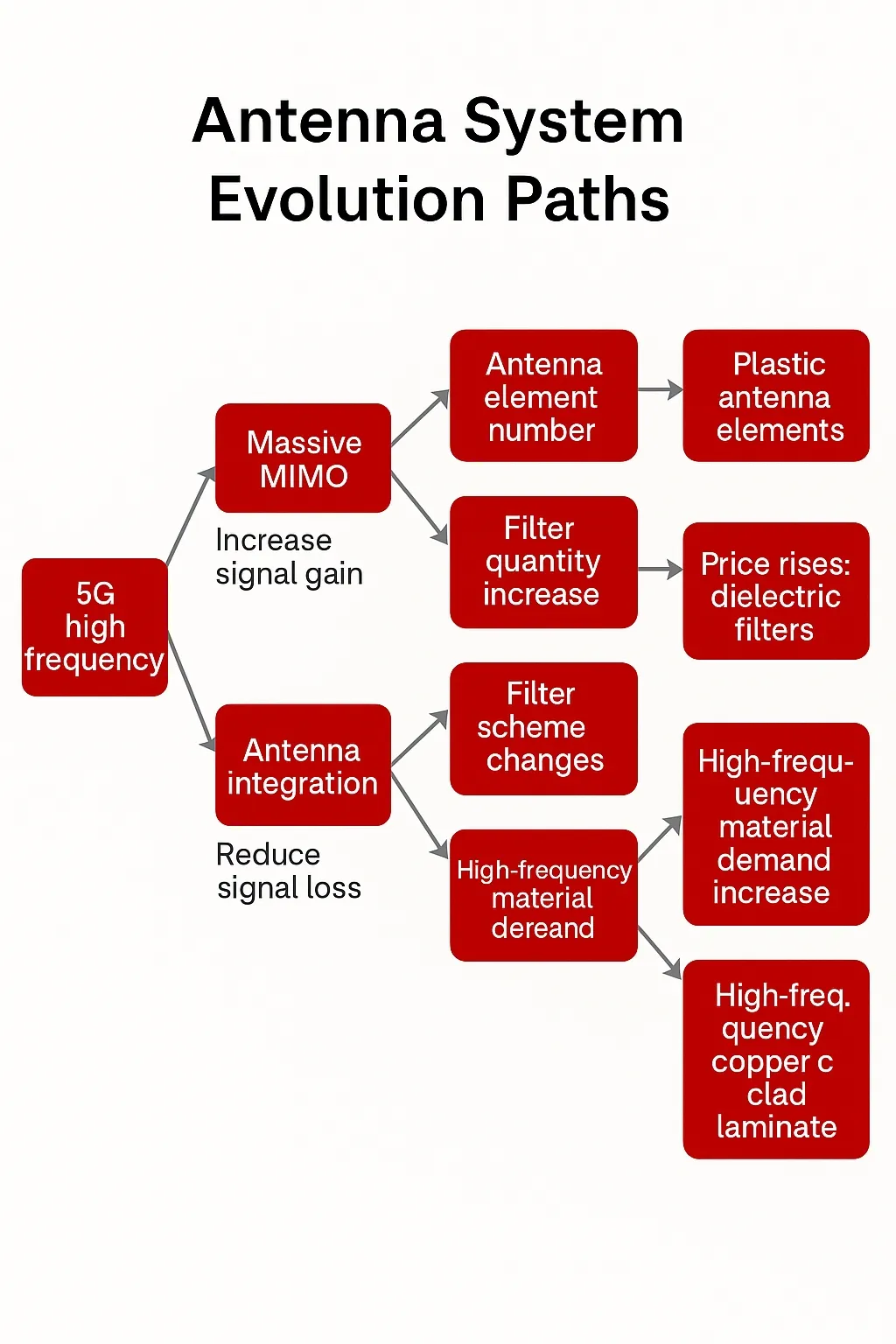

Technology evolution of 5G antenna materials

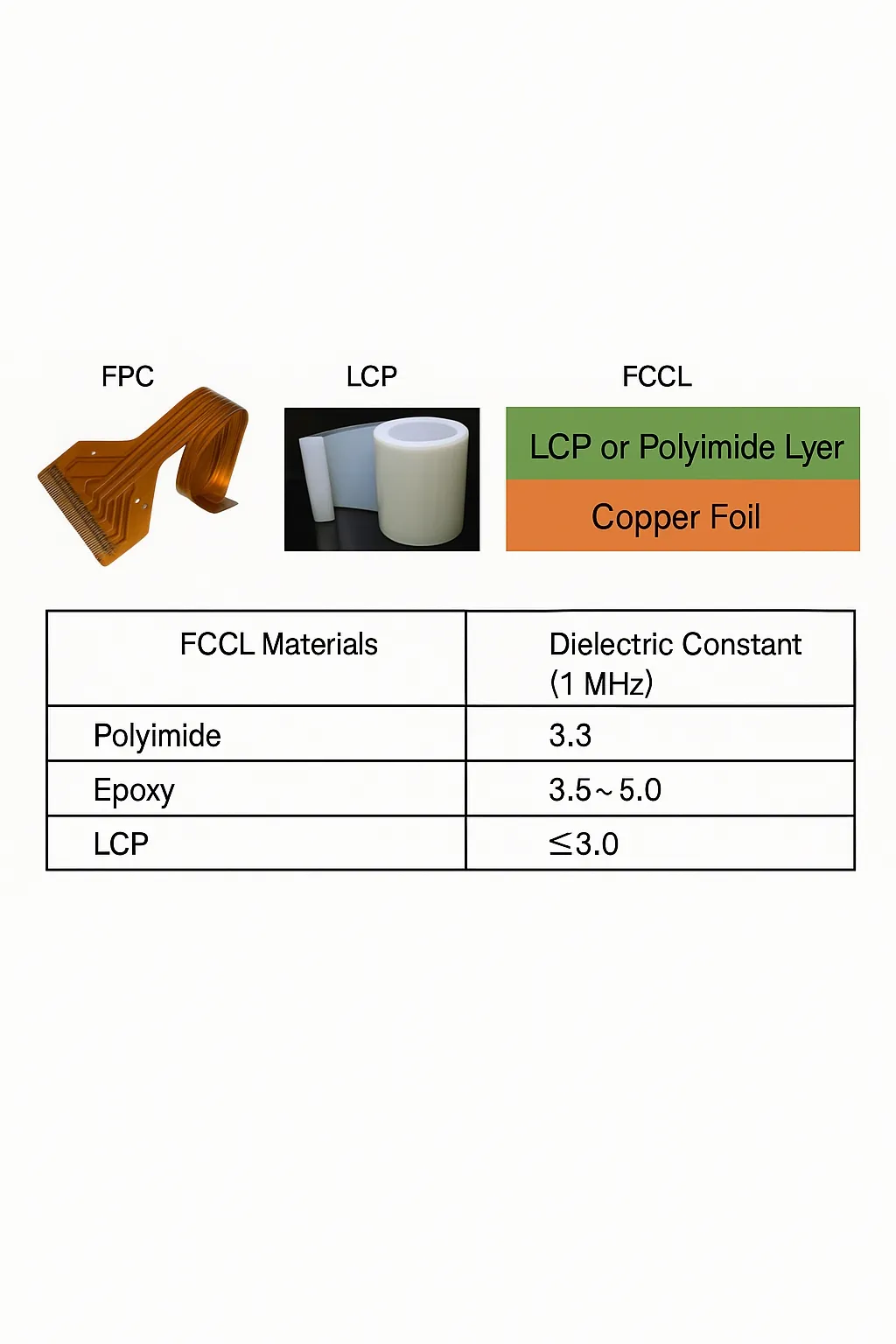

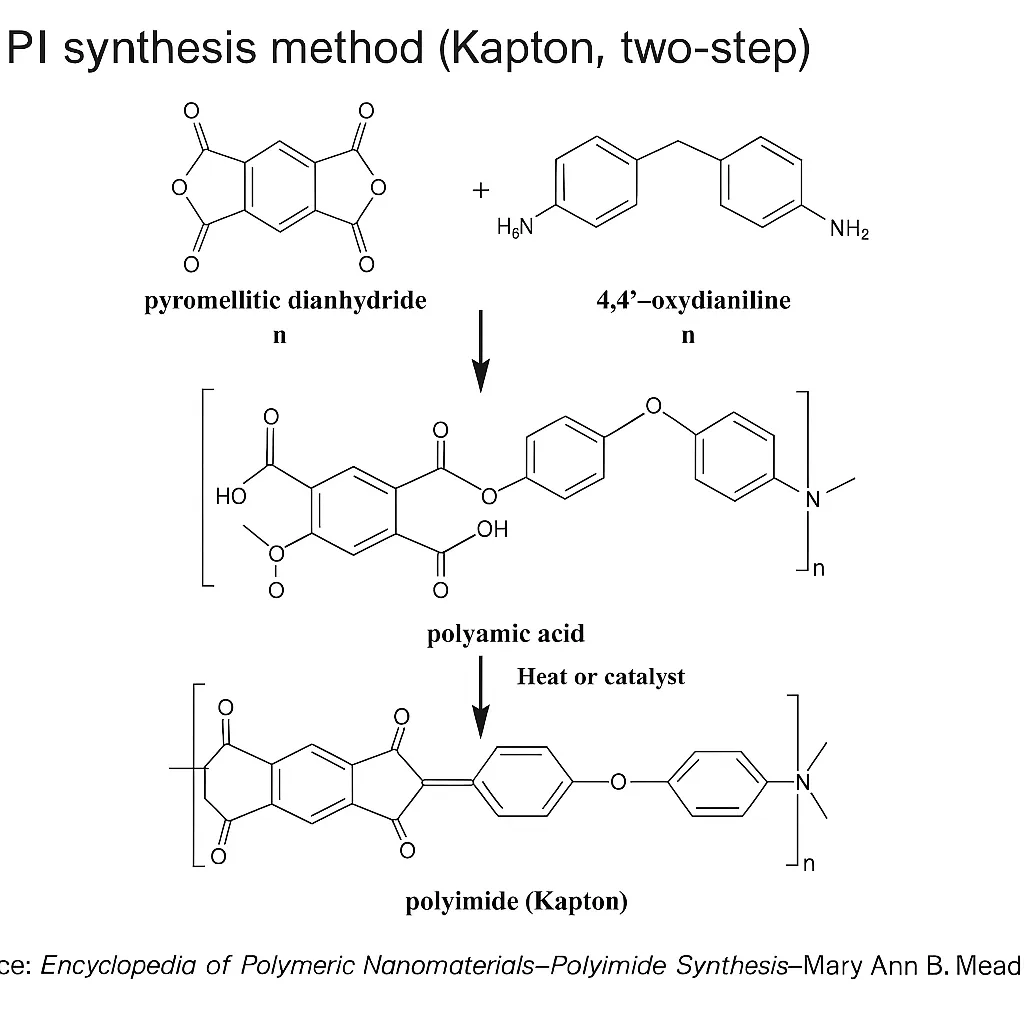

Common mobile terminal antennas built on flexible printed circuits (FPC) were made with polyimide (PI) films encapsulating copper. In high-frequency, high-speed environments, heat accumulation can cause antenna deformation, resulting in transmission loss and waveform distortion that degrades throughput.

To address this, manufacturers have explored alternative material paths such as liquid crystal polymer (LCP) and modified polyimide (MPI).

4. 5G smartphone antenna materials — LCP and MPI

Rising radio frequencies in mobile communications increase attenuation in transmission media, so antenna materials must exhibit lower loss at higher frequencies.

Early antennas used metals and alloys. With the advent of FPC processes in the 4G era, PI films became common. However, PI shows significant loss above 10 GHz and cannot meet 5G terminal requirements. LCP (liquid crystal polymer) offers lower dielectric and conductor losses, flexibility, and sealing, and has been increasingly adopted.

Because LCP is costly and the processing is complex, MPI (modified polyimide) is considered a promising mainstream choice for early 5G-era antenna materials.

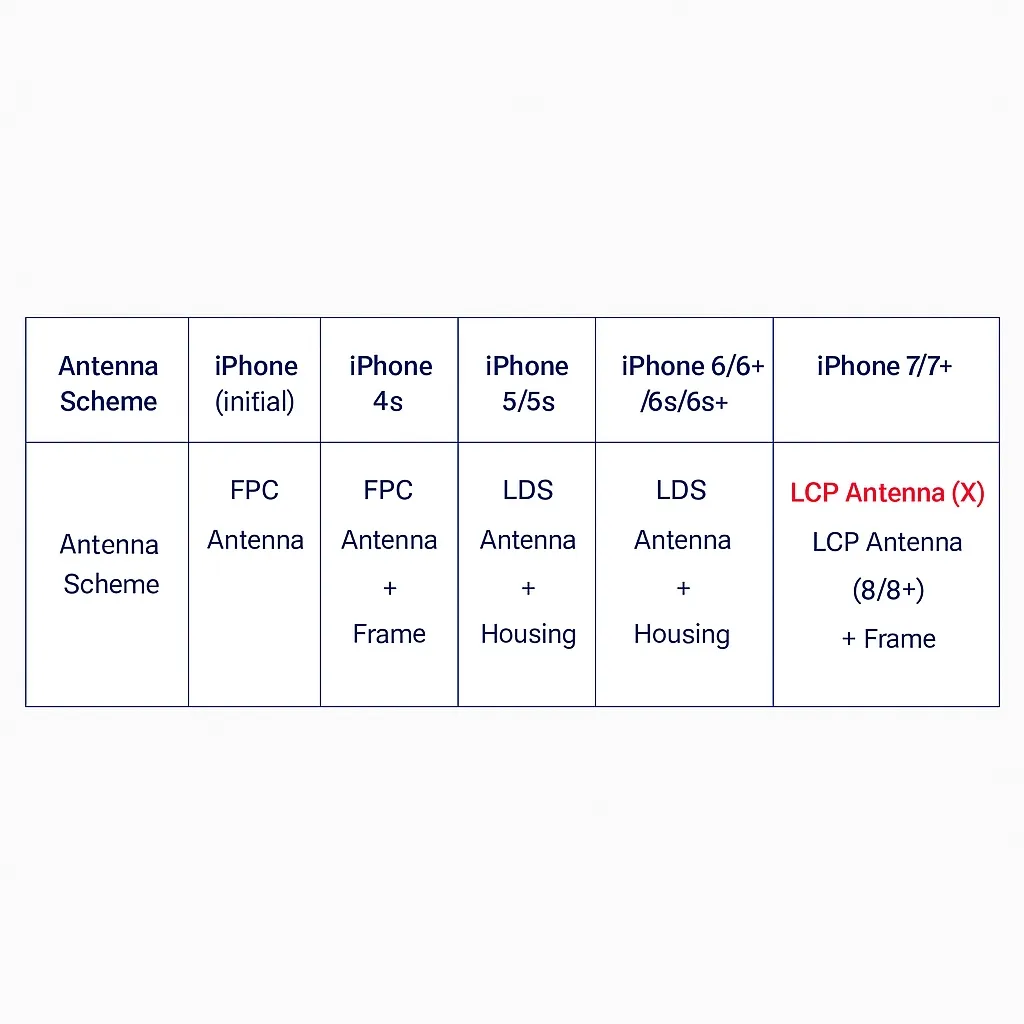

LCP and MPI characteristics

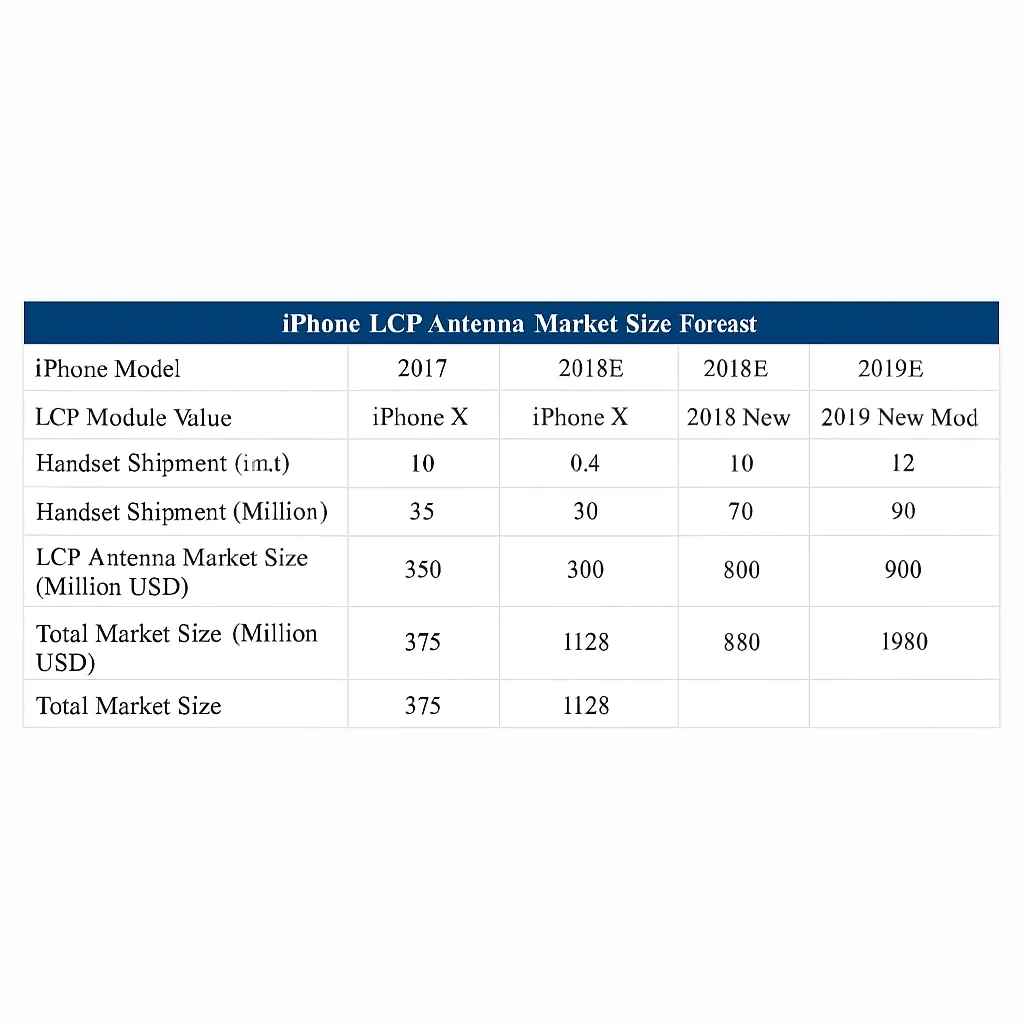

iPhone X first used two LCP antennas to improve high-frequency, high-speed performance and reduce space occupation.

Following this example, other smartphone vendors are expected to adopt LCP antennas, which could drive market expansion for LCP-based smartphone antennas.

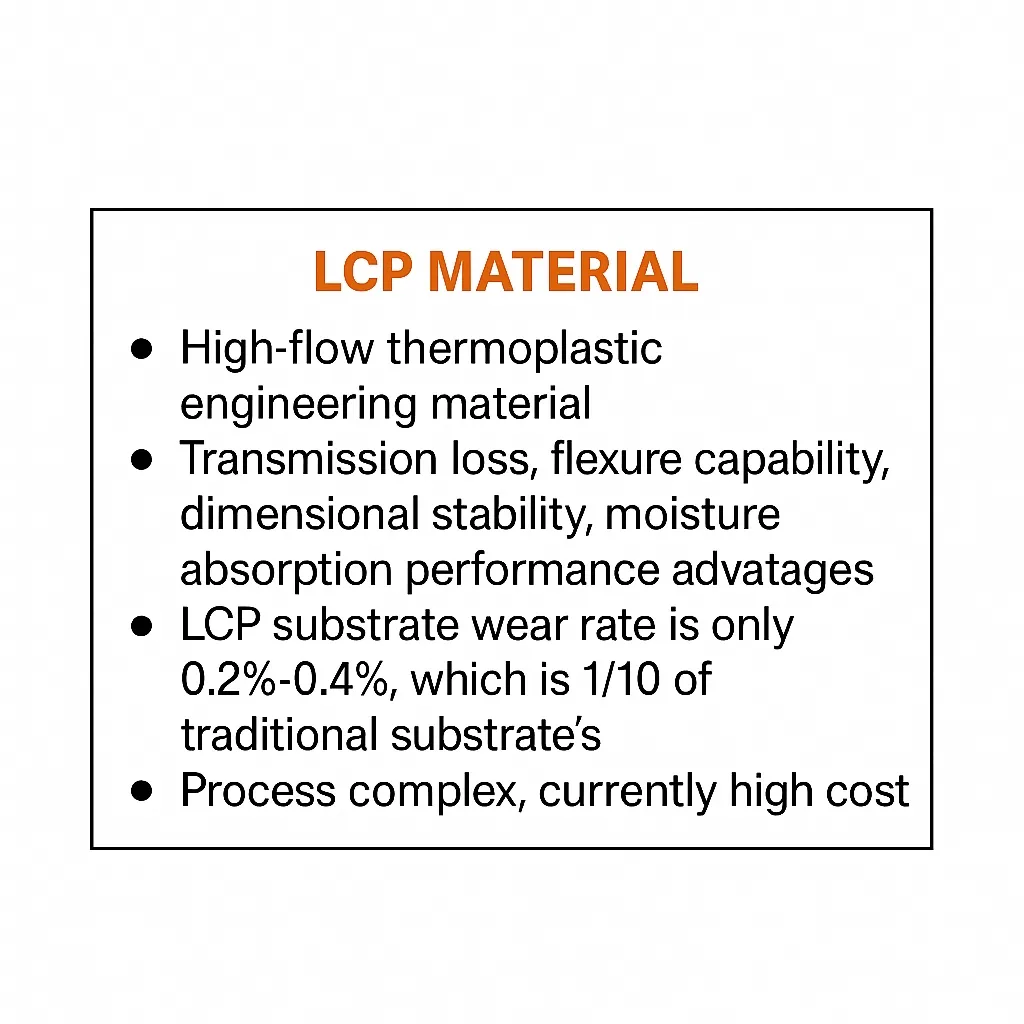

5. LCP materials

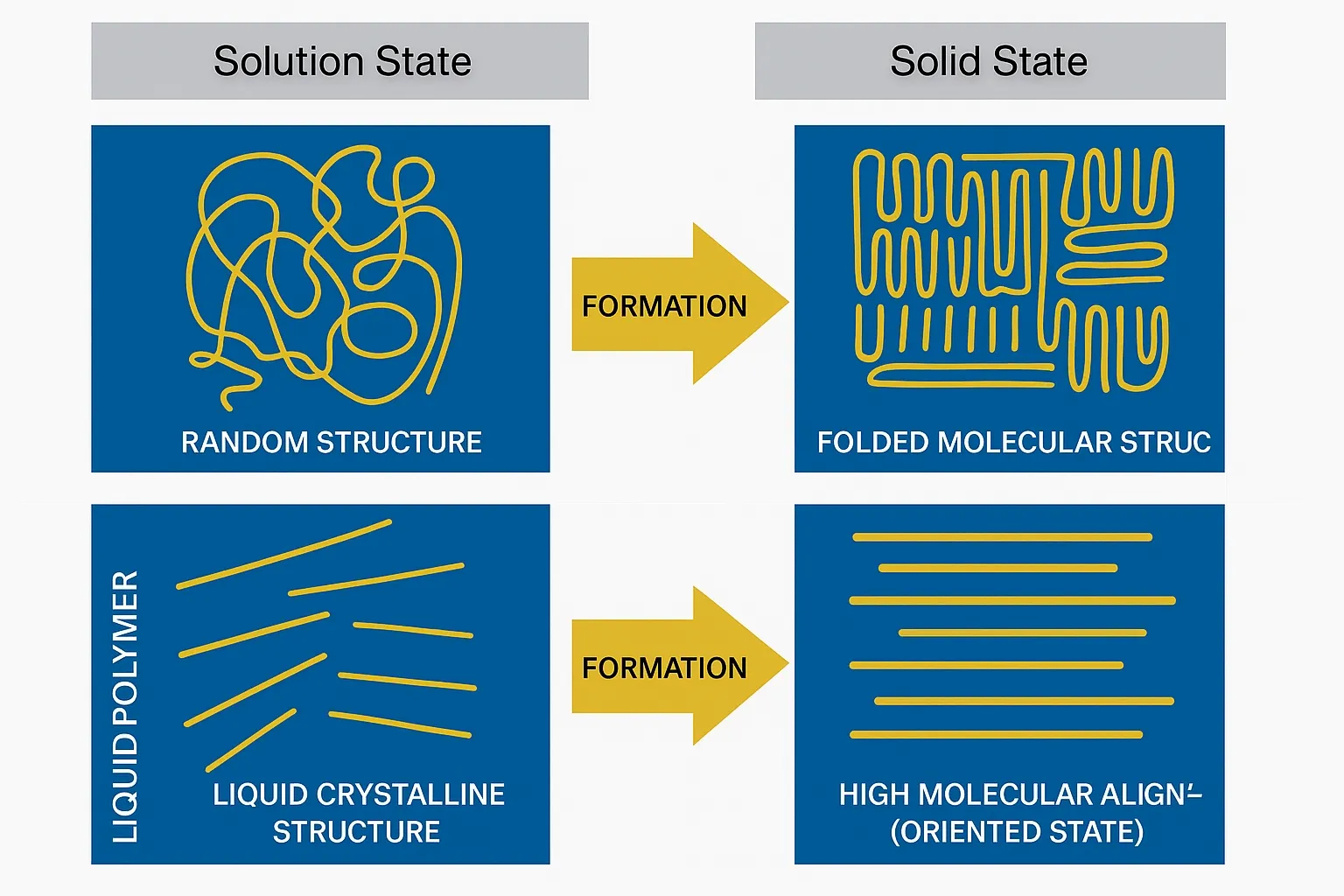

LCP stands for liquid crystal polymer. It is a polymer whose rigid molecular chains can exhibit liquid crystal behavior under certain conditions, combining fluidity and anisotropic crystalline properties.

Compared with other organic polymers, LCP has a unique molecular structure and thermal behavior. In the melt state, LCP molecules align like rods. During molding, shear stress further orients the molecules, producing strong anisotropy and a self-reinforcing effect. This ordered structure gives LCP excellent mechanical strength, dimensional stability, optical and electrical properties, chemical resistance, inherent flame retardancy, good processability, heat resistance, and low thermal expansion coefficient.

Because the main chain motion is restricted by the molecular backbone and liquid crystal structure, LCP shows very low dielectric constant and dielectric loss at high frequencies.

Given the increasing dielectric performance demands in 5G devices, LCP’s properties make it well suited for high-speed connectors, 5G base station antenna elements, 5G smartphone antennas, and high-frequency circuit boards.

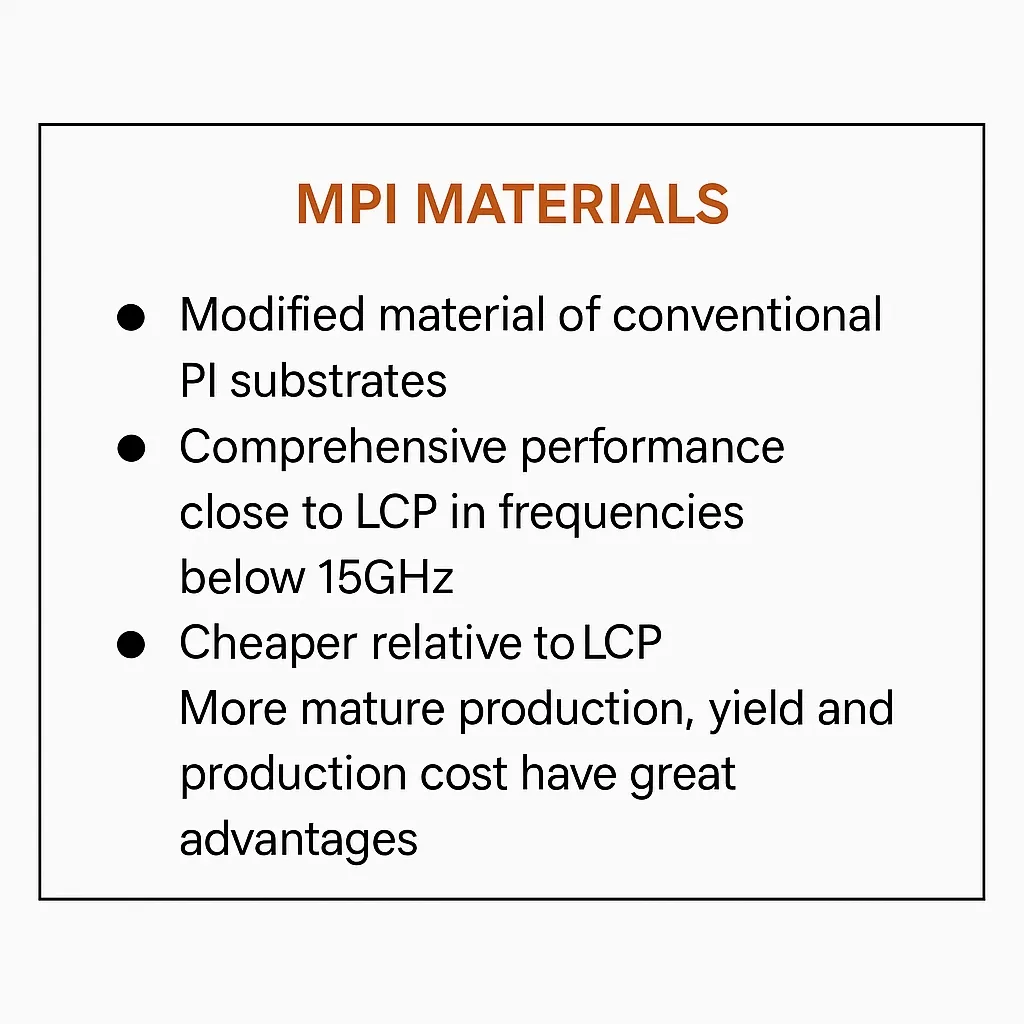

6. MPI materials

MPI refers to modified polyimide formulations. Polyimide has excellent chemical resistance, mechanical strength, and high electrical resistivity, which has led to widespread use in microelectronics and aerospace. Compared with traditional inorganic materials, polyimide offers advantages in planarization and ease of processing, making it a common choice for electronic assemblies.

As an amorphous material, MPI has a wide processing temperature window, is easy to handle during low-temperature copper lamination, adheres readily to copper, and is relatively cost-effective.

With fluorinated formulations, MPI performance at 10–15 GHz can approach that of LCP. Some industry participants therefore consider MPI sufficient for many 5G applications, competing directly with LCP. Certain North American manufacturers have adopted MPI in part because of LCP production capacity constraints.

In summary, LCP may ultimately be a major 5G winner, but during the 4G-to-5G transition, MPI has a realistic opportunity to gain share.

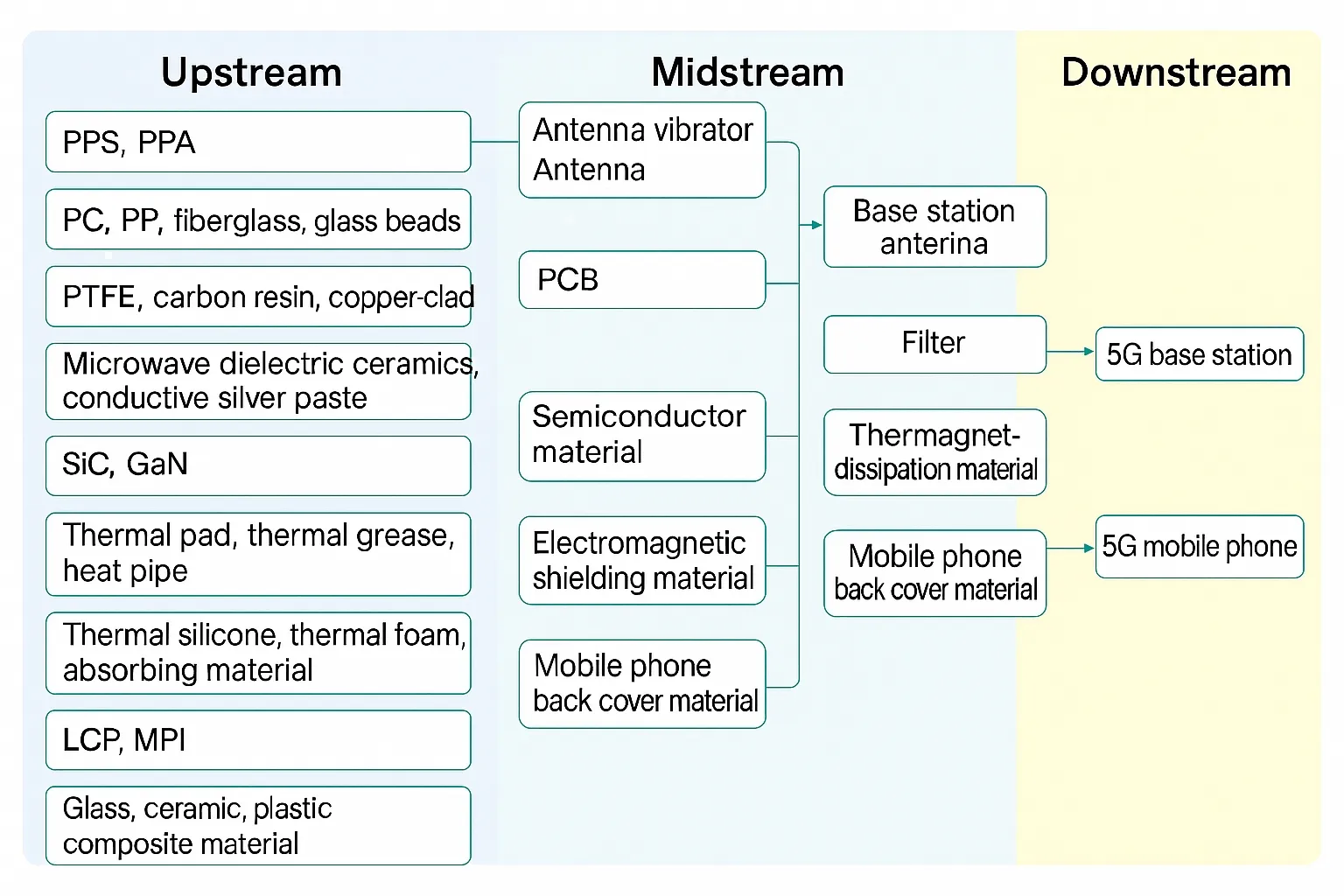

7. LCP antenna materials industry chain and structure

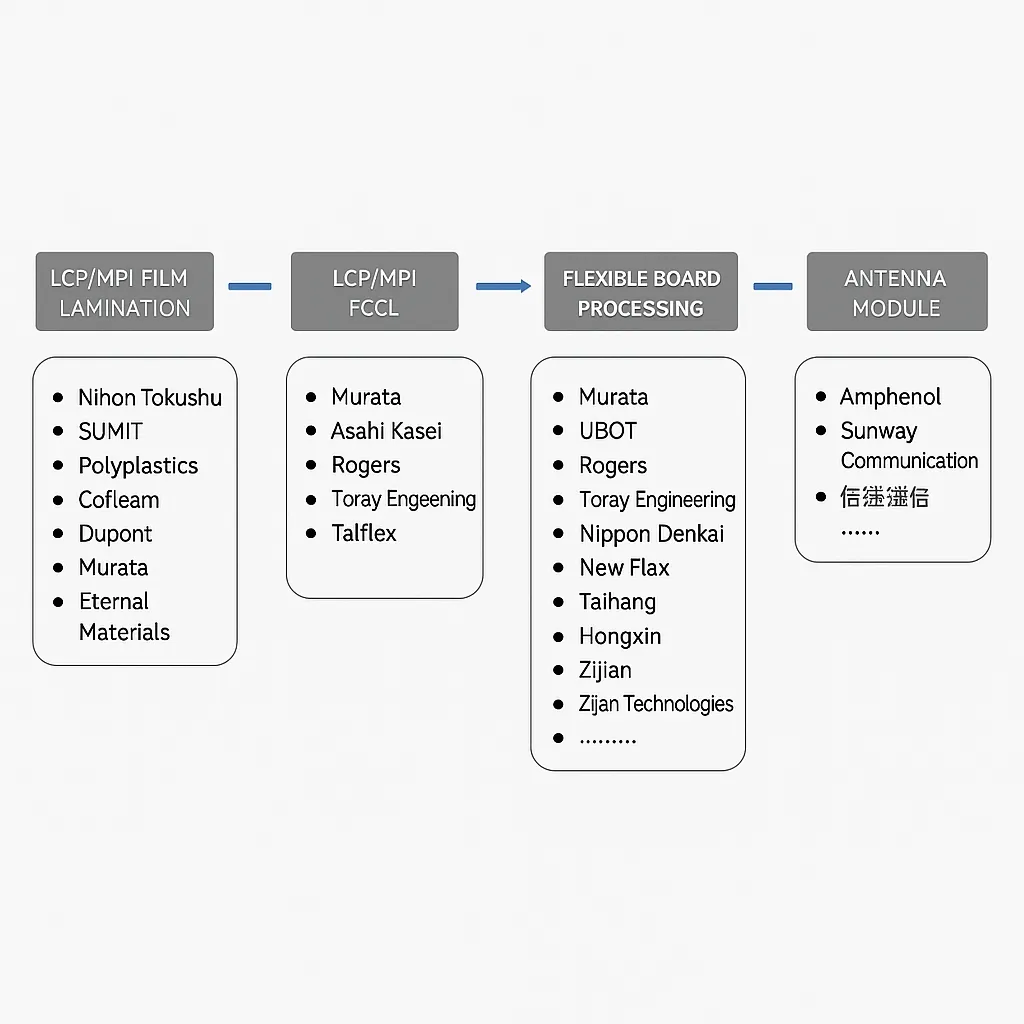

The LCP antenna industry chain consists of upstream raw material suppliers and FCCL (flexible copper-clad laminate) manufacturers, midstream FPC flexible board manufacturers, and downstream antenna module manufacturers. Upstream raw materials include LCP resin/film and rolled copper foil. FCCL manufacturers use these inputs to produce FCCL. FPC manufacturers process FCCL into flexible circuit boards, and antenna module manufacturers convert FPC into antenna modules according to design. Multiple stages in the LCP antenna chain have high technical barriers; the most difficult are film-grade LCP resin synthesis and film stretching.

(1) LCP resin synthesis is complex. Several monomers participate in synthesis, typically requiring melt polymerization and solid-phase polymerization steps. Strict control of impurities and molecular weight distribution is necessary, and specialized equipment is required. Among synthesis routes, the methods used by Baoli and Celanese are considered favorable for film stretching.

(2) Film forming is technically demanding. Film production requires extensive practical know-how, and closed supply chains between resin producers and film manufacturers make it difficult for new entrants to obtain film-grade resin or produce qualified films. Successful industry combinations include Baoli-Kolon (blown film)-Panasonic Electric Works and Baoli-Murata (double draw). Sumitomo and other Japanese firms are also involved. Post-film processing steps such as thermal treatments and coatings contain significant proprietary know-how.

(3) Other steps: FCCL production involves copper lamination, and LCP’s thermoplastic properties demand precise temperature control for that process. Drilling vias in LCP-based flex circuits is challenging due to multilayer constructions. Mechanical drilling methods used for traditional FPC are not suitable. Murata uses buried capacitor and buried inductor techniques, while some Taiwanese suppliers use laser drilling. Globally, only a few companies can mass-produce film-grade LCP resin; Baoli in Japan and Celanese in the US have capabilities, with Murata and other firms commercializing film processes.

Competitive landscape

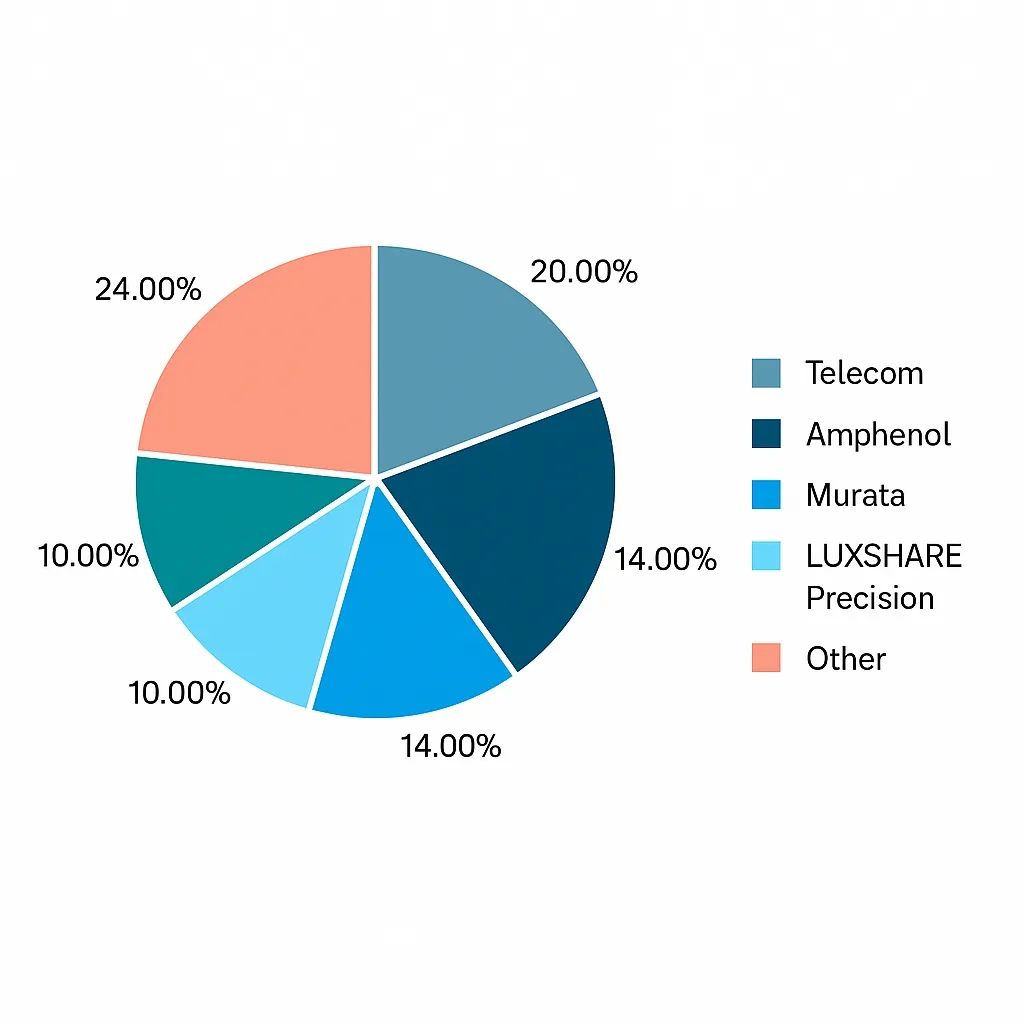

Global antenna terminal markets show an oligopolistic structure: the top eight firms capture over 85% of the global market, with five of the top eight based in China and holding more than 60% market share collectively. Major international vendors include CommScope (Acquired Andrew), Korea-based ACE, and Kathrein. In mobile terminal antenna components, leading suppliers include Amphenol, Molex, Luxshare Precision, Sunway Communication, and Sunway’s competitors.

LCP antenna industry chain details

The industry chain includes upstream LCP resin/film suppliers and FCCL manufacturers, midstream FPC manufacturers, and downstream antenna module makers. LCP film production and film-grade resin synthesis are the most technically challenging links.

(1) LCP resin synthesis is highly demanding, involving multiple monomers and multi-step polymerization. The process requires tight impurity and molecular-weight control and specialized equipment. Baoli and Celanese synthesis routes are favorable for film formation.

(2) Film manufacturing requires extensive practice and is protected by closed supply chains; new entrants face difficulty sourcing film-grade resin and producing qualified films. Successful commercial film technologies are limited to a few companies with mature applications.

(3) Other process steps, such as copper lamination for FCCL and via formation on LCP flex, present additional technical challenges. Laser via drilling and specialized embedded component techniques have been developed to address these issues.

Companies mastering LCP film technology

Core LCP film technology is concentrated among a few Japanese and U.S. companies, with only a subset having achieved full commercial maturity. Firms with relevant capabilities include Superex (U.S.), Murata (Japan), Kolon (Japan/Korea), and Chiyoda (Japan). Murata and Kolon are noted for reaching commercial maturity in antenna-grade LCP films.

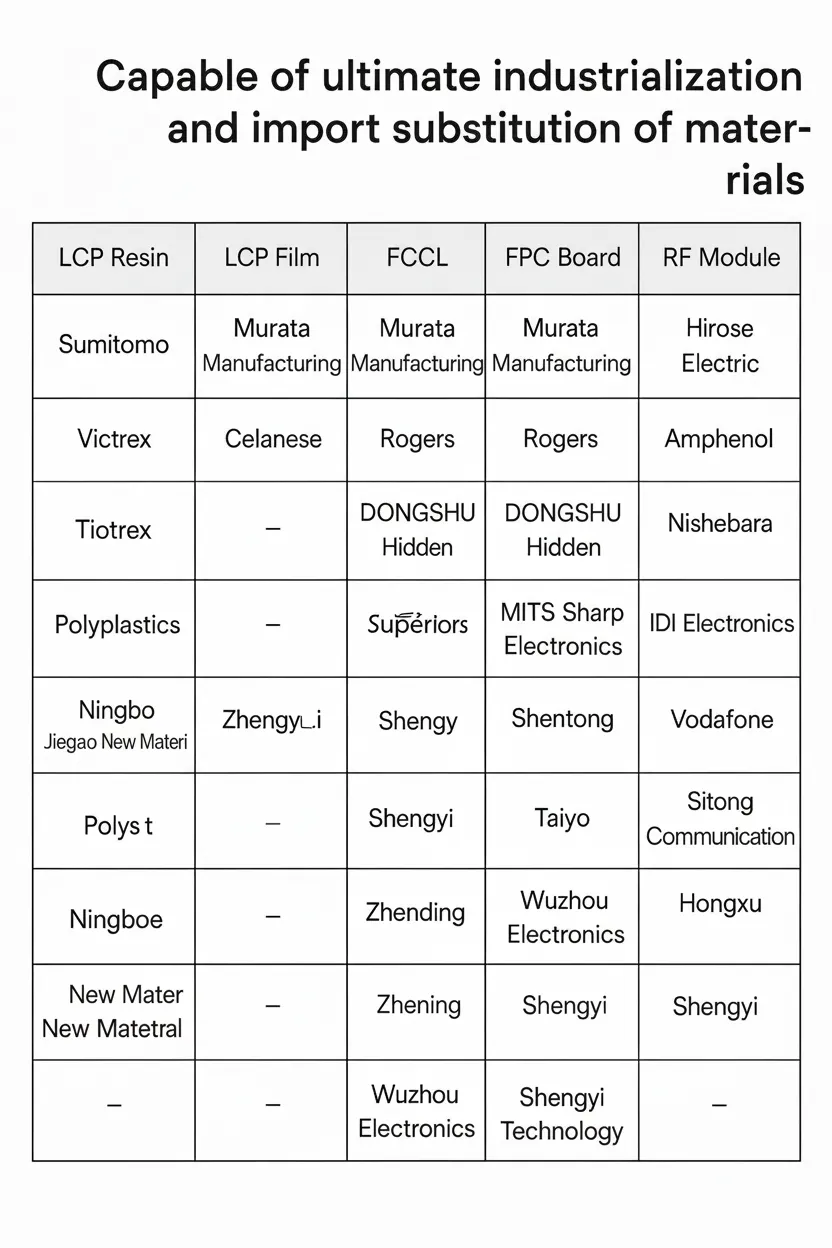

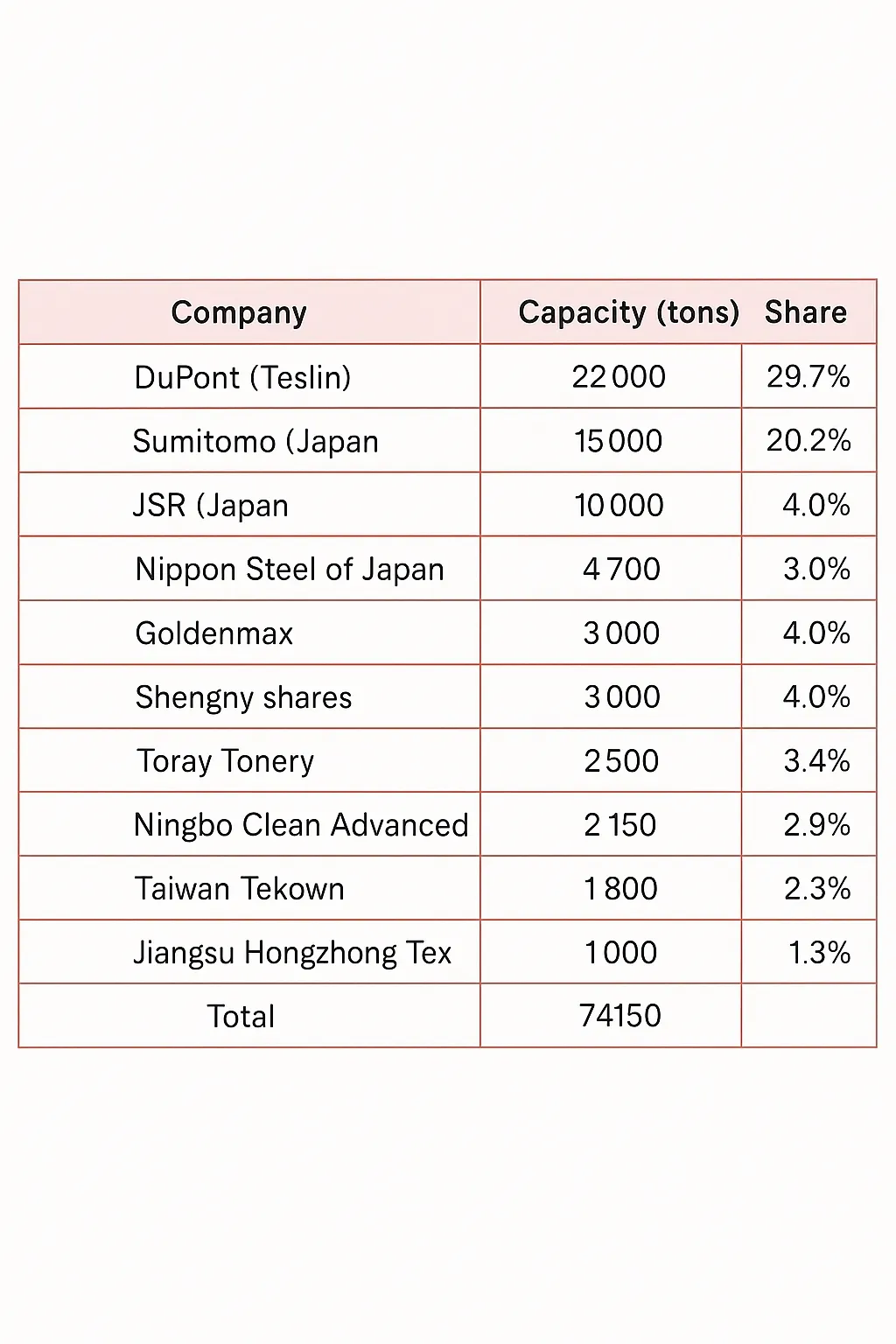

Global LCP resin production is mainly in the U.S. and Japan. Major suppliers include Celanese, Polyplastics (Baoli), and Sumitomo, which together account for approximately 63% of global capacity. Celanese’s acquisition of DuPont’s LCP business increased its global capacity to around 22,000 tons, near 30% market share. Other companies are developing film-grade resins to meet production needs.

LCP resin/film producers and industrial progress in China

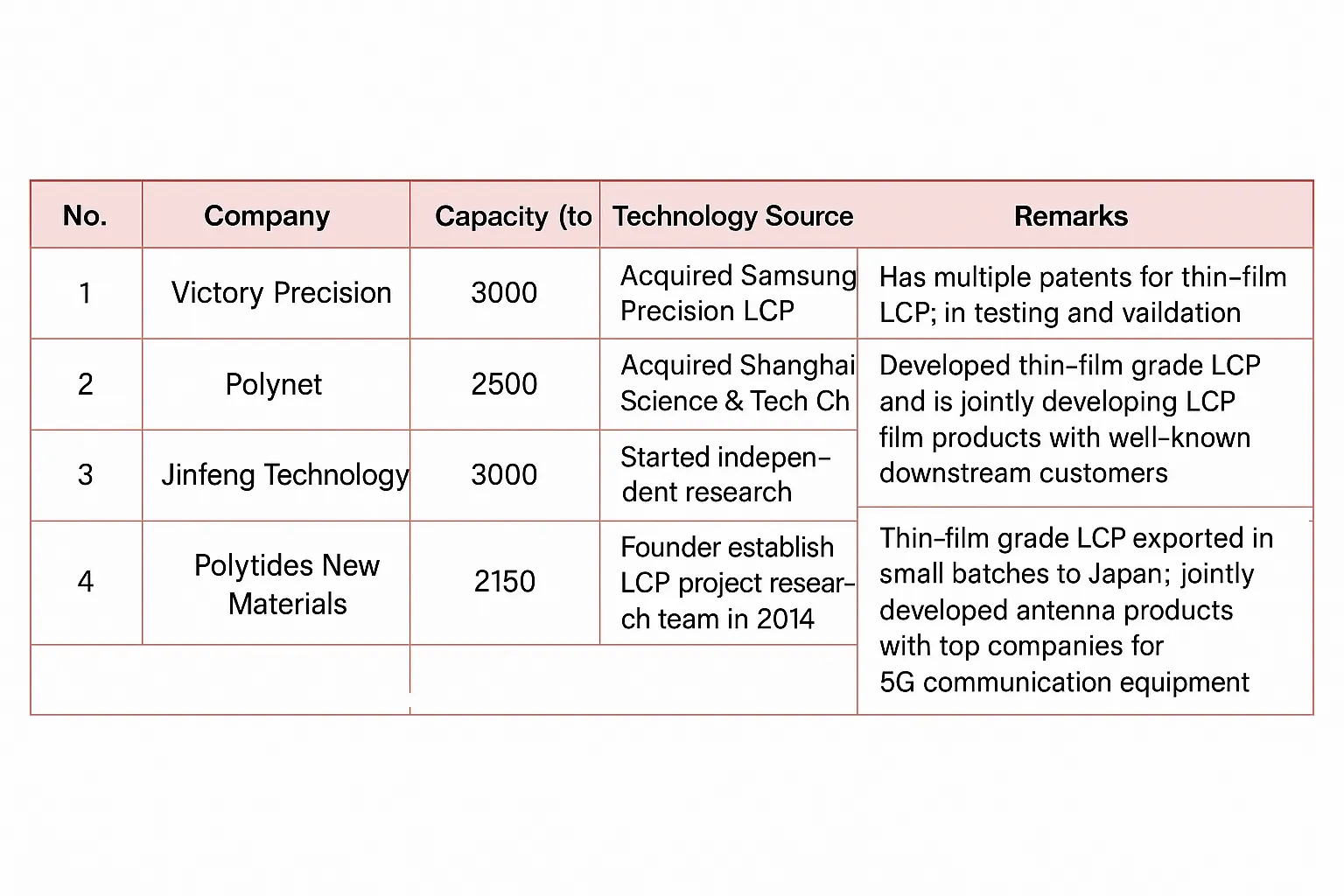

From an industrialization perspective, currently there is no company in China that can independently mass-produce antenna-grade LCP film or film-grade LCP resin at scale. However, several Chinese companies have made progress in resin and film development and small-volume supply.

Notable developments among Chinese and Taiwan-related players include:

- Wote Co., Ltd.: Film-grade LCP is in testing and is entering batch supply as downstream customers complete qualification. The company focuses on modified engineering plastics, high-performance polymers, carbon-fiber composites, and fluoropolymers. Its LCP and PTFE series products rank highly in technical capability, and the company reported revenue growth in recent annual reports. The company acquired an LCP production line originally owned by a Korean firm and reports testing of film-grade resins with customers.

- Kingfa Sci. & Tech: Small-volume exports of film-grade LCP resin have been reported, and collaboration with 5G equipment vendors on antenna products is underway. Kingfa has been developing LCP since 2009 and aims to expand capacity significantly. The company reports small-volume shipments to Japan and technical cooperation with domestic 5G equipment manufacturers.

- Pliteq: Successfully developed film-grade resin and is jointly developing LCP film with downstream customers. Pliteq has a strong position in automotive modified plastics and global operations. It has developed injection-grade, film-grade, and fiber-grade LCP resins, with injection-grade materials already supplied to customers.

- Ningbo JuJia New Materials: Claims film-grade LCP resin production capability and is piloting film products. The company established production lines with capacity claims for film-grade resin and is in pilot-scale film trials.

As Chinese companies continue R&D and process improvements, bottlenecks for mass-producing antenna-grade LCP film may be overcome; progress in industrialization and customer qualification will be important to monitor.