ALLPCB

ALLPCB

China medical electronics market size and outlook

In recent years, driven by rising health needs and health spending among residents, the rollout of community and rural medical services, and rapid demand for basic and emergency medical equipment, China’s portable medical electronics market has expanded rapidly.

In 2015 China's portable medical electronics market reached RMB 57.74 billion, a year-on-year increase of 21.43%. In 2016 it reached RMB 68.53 billion, a year-on-year increase of 18.69%. The recent scale of China’s portable medical electronics market is shown in the figures below.

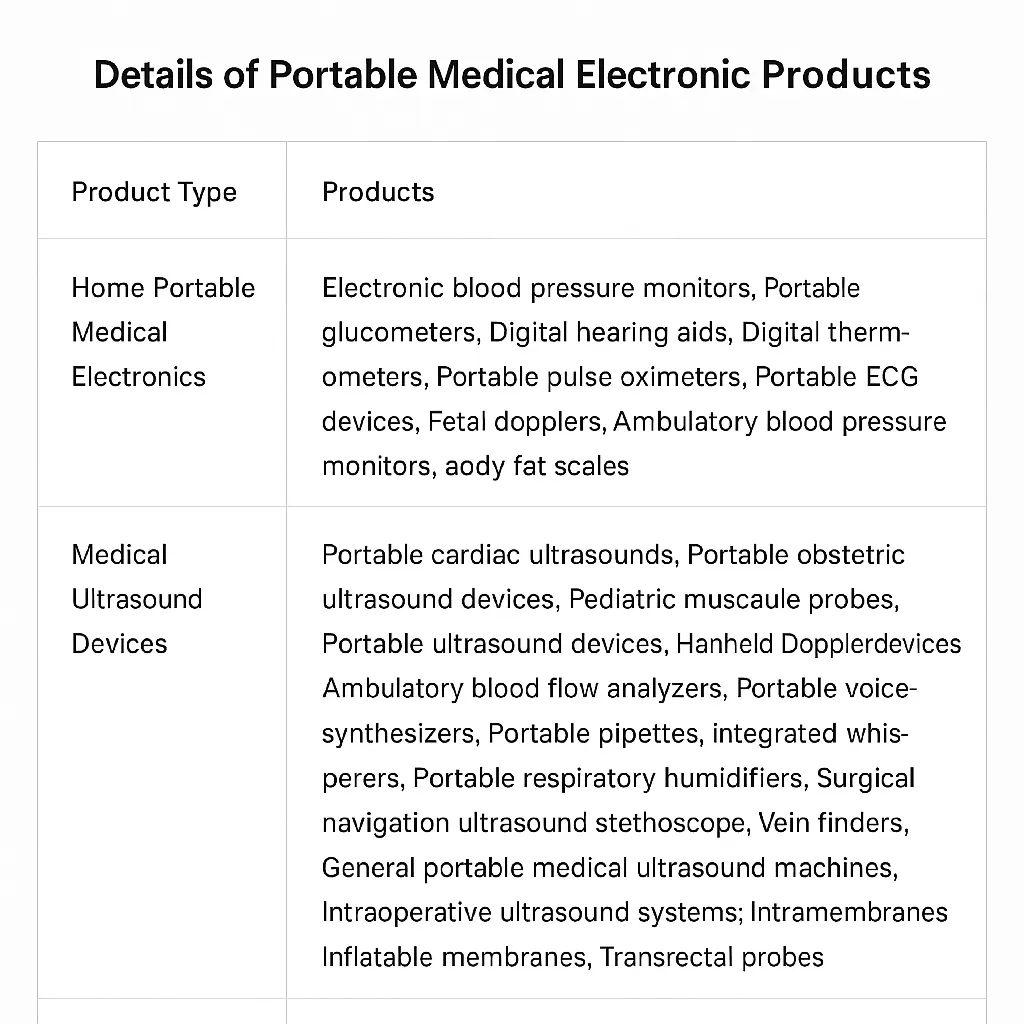

Portable medical electronic products are divided into two main categories: consumer portable and clinical portable. Consumer portable products include portable electronic blood pressure monitors, portable blood glucose meters, and digital thermometers. Clinical portable products include portable cardiac defibrillators, ambulatory electroencephalographs, multi-parameter portable monitors, and portable ultrasound diagnostic devices.

In the coming years, as China’s population continues to age, demand for portable medical electronics is expected to keep growing rapidly. Forecasts indicate China’s portable medical electronics market will maintain about 14% growth annually and reach RMB 172.31 billion by 2023, as shown below.

China semiconductor industry status and outlook

The semiconductor industry is often described as a national industrial jewel and reflects a country’s comprehensive industrial strength. A semiconductor is a material whose electrical conductivity at room temperature lies between that of a conductor and an insulator. From both technological and economic perspectives, semiconductors are critical. Most modern electronic products, such as computers, mobile phones, and digital recorders, rely closely on semiconductor components.

The semiconductor industry is known for high added value and a wide range of products, mainly including integrated circuits (ICs), discrete devices, optoelectronic devices, and micro sensors. Integrated circuits are the core of the semiconductor industry. According to the World Semiconductor Trade Statistics, global IC sales reached US$276.7 billion in 2016, accounting for 82% of the semiconductor market. Due to technical complexity, the industry structure is highly specialized. As the industry scales rapidly, competition intensifies and division of labor becomes more detailed.

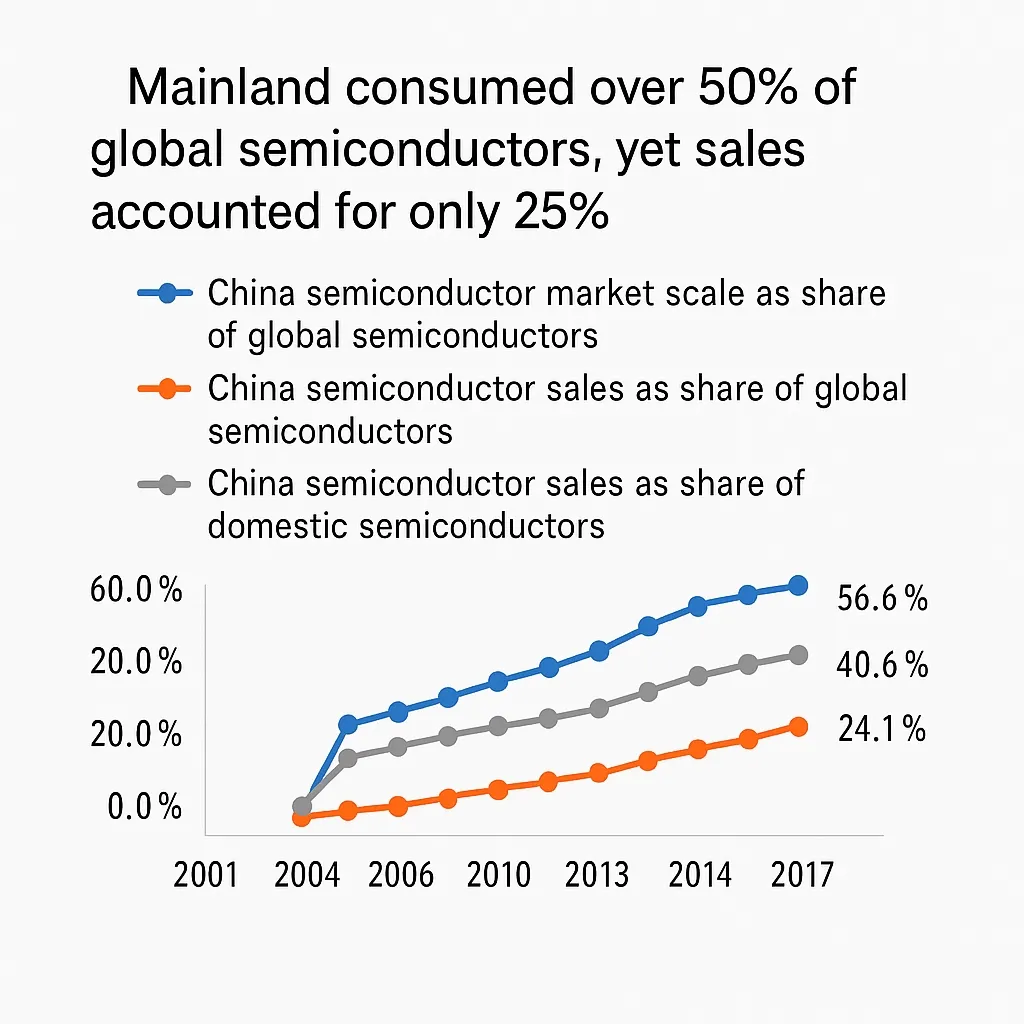

At present, the Chinese market accounts for more than 56% of global semiconductor consumption, but sales generated within China account for only about 24% of global semiconductor sales. By 2014, China’s share of global semiconductor consumption rose from 21% ten years earlier to 56%, while China’s semiconductor sales still represented only 24% of the world total, showing a mismatch between consumption and domestic sales capacity.

Equipment sales have not kept pace with China’s rapid market growth. In 2015, the semiconductor equipment market in mainland China reached RMB 30.46 billion (US$4.90 billion), of which domestic integrated circuit equipment sales were only RMB 2.292 billion, less than 8%. The domestic equipment market is still dominated by foreign companies such as Applied Materials, Lam Research, Tokyo Electron, Advantest, and KLA-Tencor, and the weak position of domestic equipment makers needs to change urgently. Mainland manufacturers are expected to be the main drivers of global capital expenditures in the next phase: of 62 planned or under-construction front-end wafer fabs scheduled for 2017–2020, 26 are located in mainland China, accounting for 42% of the global total. North America follows with 10 fabs planned for 2017–2020, *** ranks third with 9 fabs. Europe, South Korea, and Japan total 17. Of the mainland fabs, six were expected to start production in 2017 and production was projected to peak in 2018 with 13 fabs joining operations; many of the fabs completing in 2018 are wafer foundries.

Zhou Zixue commented that these years are a good starting period for responding to the market boom, but work should be low-key and steady. The semiconductor industry requires hard work to succeed.

"China’s semiconductor competitiveness is still weak. There are no Chinese companies among the global top 20 semiconductor firms. In specific segments, we basically have no CPUs; we have very few logic devices; memory companies are still under development and products have not yet emerged; equipment and materials companies are even weaker. Across segments, our competitiveness is insufficient. Second, resources are dispersed; the industry lacks concentration. Third, excessive publicity has raised vigilance in some countries. We need to work solidly and persistently; excessive publicity will create more obstacles," Zhou said.

Regarding the future development of China’s semiconductor industry, Zhou provided a rough timeline. By segmenting the value chain, China could develop design and packaging into relatively technical sectors in 5–10 years with persistent effort. In 10–15 years manufacturing and some materials sectors could reach relatively high levels. "As for critical equipment manufacturing, even in 30 years China may not be able to produce the world’s most advanced semiconductor equipment," Zhou emphasized. He noted that the industry is international and no country leads end to end. If after 20 years some Chinese semiconductor companies become internationally competitive, that would be success. The process should start with R&D and requires sustained government support; intermittent support will not succeed.

Relationship between China’s medical electronics market and the semiconductor industry

1. The Chinese medical electronics market as a major opportunity

In recent years, driven by global population aging, rising living standards, and government policy and investment in healthcare, the global medical electronics market has grown rapidly. In 2016 global medical electronics sales reached US$253.47 billion, of which China accounted for 11.48%, making it the third-largest market after the United States and Europe.

There is a large equipment gap in the Chinese medical device market. It is estimated that over 60% of instruments and equipment in national healthcare institutions are products from before the mid-1980s, implying that most existing devices need replacement. Portable medical electronic products used in homes and clinics have become a fast-growing segment of the medical electronics market. In addition, medical device and pharmaceutical consumption per capita in China is far below that of developed countries, indicating significant potential market growth.

Advances in electronics have enabled new medical electronic devices. Compared with consumer electronics, which can form bubbles and fade quickly, medical electronics is a relatively stable market. Although time from development to certification is long, the market potential and stable returns attract many semiconductor companies. Medical applications have become one of the fastest-growing areas for semiconductor markets.

2. Portable and wearable devices are a hot segment

Medical electronic devices are extending functionality toward therapy, analysis, rehabilitation, and wellness. Although diagnostic lab equipment, monitors, implantable insulin pumps, and pacemakers remain the largest revenue areas, societal development and rising health awareness increase demand for management and diagnosis/treatment of chronic diseases, disabilities, and neurological disorders. Consequently, preventive and wellness-oriented devices are moving into homes and personal care. Among portable medical electronics, home diagnostics is expected to account for about 50% of the market; of the remaining 50%, imaging products account for 25% and other diagnostic or therapeutic electronic products account for 25%. Wearable home wellness devices such as electronic blood glucose meters and electronic blood pressure monitors will be another strong growth driver. Wearable consumer medical products are becoming prominent in the market and are poised for rapid development.

Conversely, demand for wearables also promotes smart medical industry development. Yang Zhenglong, Asia Pacific marketing manager for ON Semiconductor's medical division, noted that remote capability, connectivity, portability, intelligence, and professional functionality are trends for wearable medical electronics. Smart wearables can record physiological parameters such as heart rate and blood pressure 24/7. Longitudinal daily data, when analyzed by professional hospitals, can help detect intermittent or hidden conditions and enable more accurate treatment. In short, wearable traits make health monitoring more convenient and simpler, supporting the continued development of medical health technology to meet market needs.

3. Opportunities and challenges for semiconductor suppliers

Semiconductor products are key to improving the core functions and performance of portable medical electronics. The intelligence, remote connectivity, and networking requirements of portable devices combine data acquisition, low-power power management, and data transmission and analysis technologies, creating opportunities for semiconductor component suppliers, device manufacturers, and service operators.

Major suppliers for medical semiconductors include Intel, Texas Instruments, STMicroelectronics, Linear Technology, Renesas, NXP, and ON Semiconductor. They primarily supply data acquisition ICs, power management ICs, power devices, sensors, MCUs, FPGAs, DSPs, and other core medical semiconductor products. Advances in semiconductor technology are accelerating medical innovation. With improvements in high-speed computing, high-precision ADCs, and wireless networking, portable and miniaturized medical electronics are becoming feasible.

For semiconductor vendors, China’s portable medical electronics market represents both opportunity and challenge. In the consumer portable field, although medical devices often have lower component performance requirements, the shift toward home-based healthcare means many devices are battery powered, making low operating voltage and low power consumption key considerations. Wearability demands small package sizes. To achieve low cost and high reliability for large volumes of diagnostic and wellness applications, high integration is a trend. For patient safety and consistent health monitoring, high precision and product consistency are crucial. Finally, wireless connectivity solutions are fundamental to device intelligence, remote capability, and portability and align with IoT device development. Suppliers such as ON Semiconductor, Renesas, and Texas Instruments are improving integrated wireless connectivity solutions. In summary, stability, high precision, high integration, low power, and wireless connectivity are primary semiconductor requirements for portable medical electronics.

Yang Zhenglong noted that wearable products face battery life and miniaturization challenges. ON Semiconductor has addressed size and power concerns through over 30 years of medical R&D investment, unique 3D packaging and system-in-package (SiP) technologies. 3D packaging connects different silicon dies and discrete components within the same package, reducing signal distances to save space and improve electrical performance. SiP can simplify micro hearing aid assembly. ON Semiconductor has also developed wireless rechargeable solutions for wearable medical devices such as hearing aids to address battery life issues.