ALLPCB

ALLPCB

Overview

In the wake of ChatGPT, demand for chips used to train and deploy artificial intelligence software has surged. At the same time, export restrictions on high-performance chips such as NVIDIA's H100 and the return of Huawei's Ascend series have brought renewed attention to the industry.

US export controls, improvements in domestic foundry capacity, and growing end-market demand could support price and volume increases for Huawei's Ascend series.

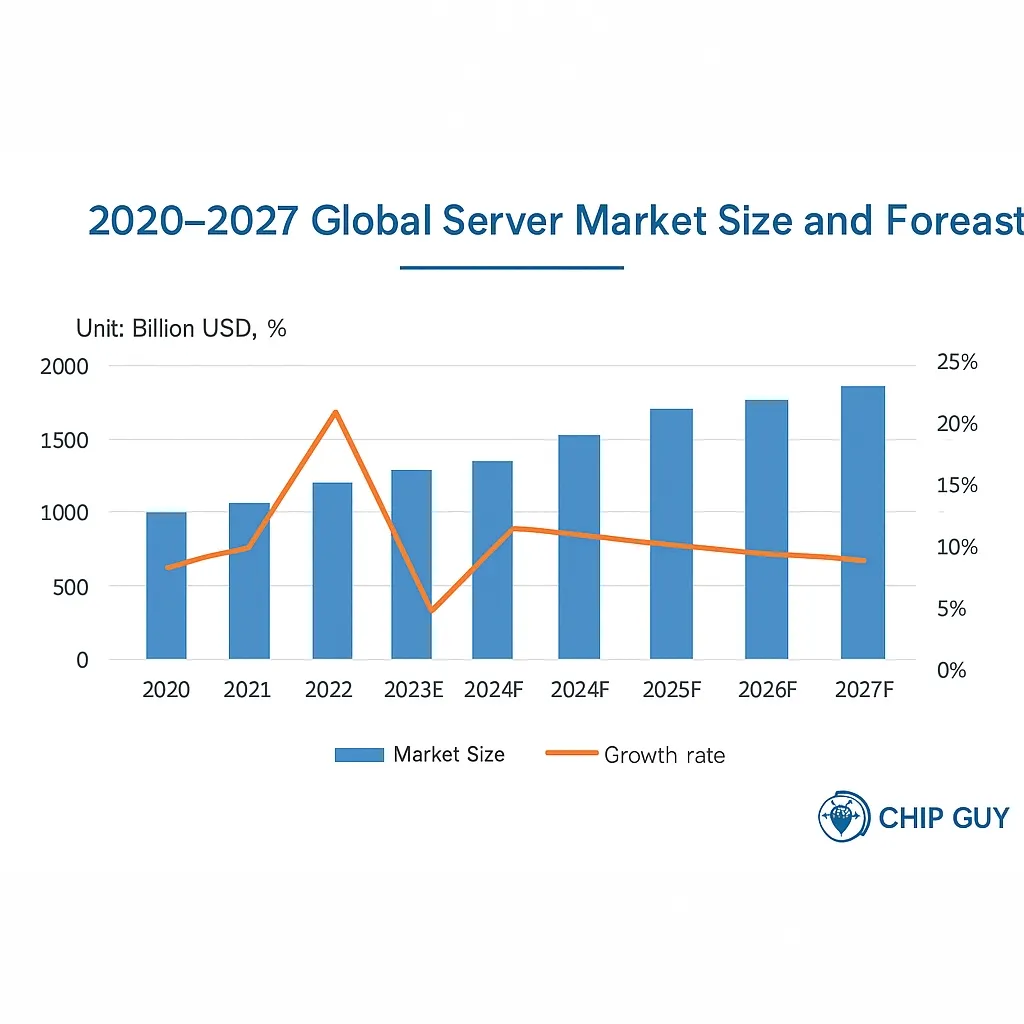

Traditional Server Slump, AI Servers Drive Market

The server market weakened this year. According to IDC latest data, by the end of 2022 the global server market reached US$123.22 billion, a year-on-year increase of 20.1%. The Chinese market accounted for more than 25%, becoming one of the main drivers of global server growth. In 2023, international developments and economic factors kept overall server demand subdued, with full-year market growth expected to slow to 4.3%.

Looking further ahead, the global server market could exceed one trillion yuan. Given rapid growth in data traffic in China and internationally and the expansion of public cloud services, servers as core compute infrastructure have significant growth potential. The market is expected to exceed one trillion yuan by 2027 (US$189.14 billion).

Source: IDC; compiled by Xinbage

AI Servers as Primary Growth Segment in 2023

Notably, with generative AI gaining traction across application areas in early 2023, AI server demand grew rapidly and has become the main growth engine for the server market. Forecasts indicate the global AI server market in 2023 was about US$21.1 billion, with shipments exceeding 1.2 million units. In China, the 2023 AI server market exceeded US$9.0 billion, accounting for more than 40% of the global market.

Domestic OEMs Lead in Server Form Factors

In the server market landscape, domestic vendors such as Inspur, HPE, and Lenovo hold relatively leading shares in server shipments and systems.

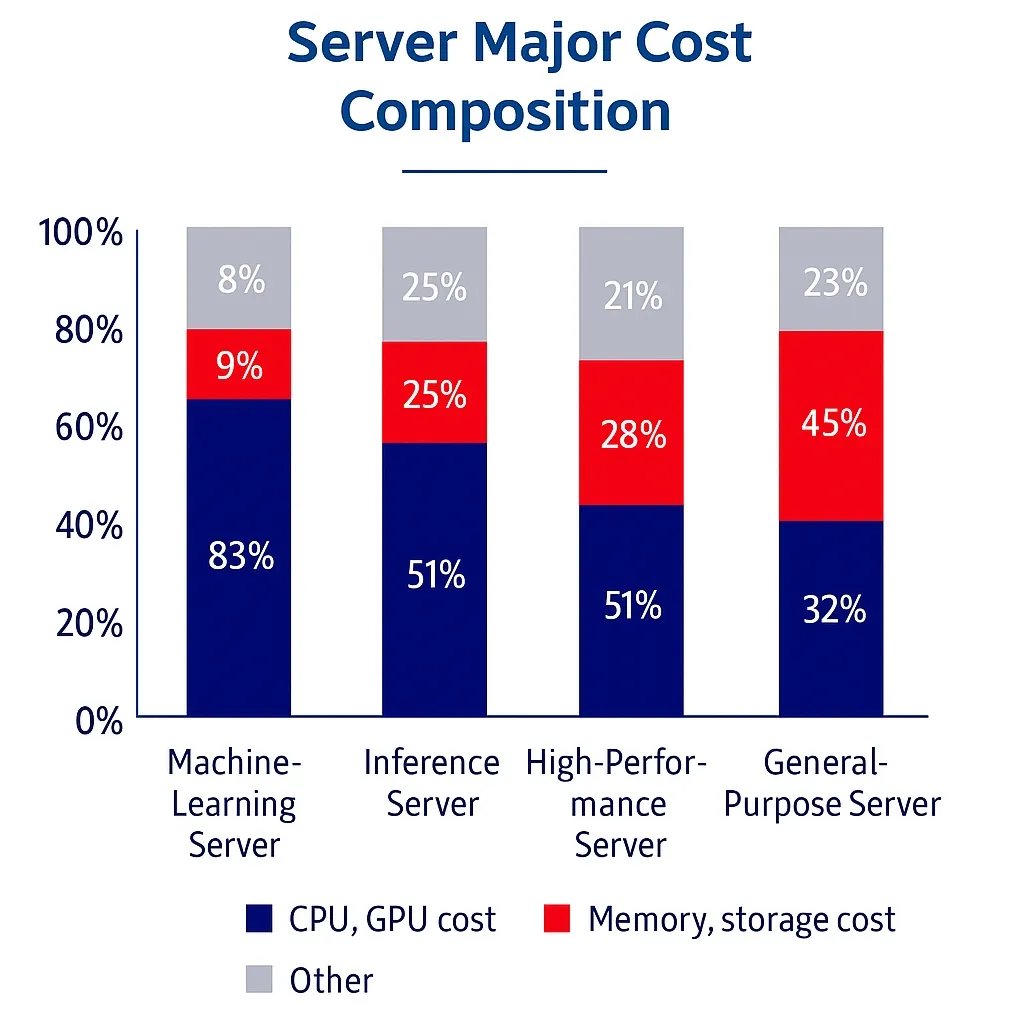

AI Chips Are the Cost Focus

Core chips such as GPUs account for the largest share of server cost. In standard servers, CPUs and GPUs represent about 30% of total server cost, but in current high-performance AI servers the share can reach more than 80%.

NVIDIA Dominates Core Server Chips

For core AI GPUs, NVIDIA holds over 90% share. NVIDIA estimated H100 GPU shipments would reach 550,000 units in 2023 and expand H100 capacity to 2 million units per year in 2024, indicating tight supply. AMD's MI300 family only began scaled production in Q4 2023, with AMD expecting 2024 shipments to reach about 10% of NVIDIA's. Domestic vendors, led by Huawei's Ascend series, have achieved some degree of substitution for overseas products. With foundry improvements and capacity increases this year, domestic orders have risen.

Across mainstream products sold in the Chinese market, NVIDIA remains dominant; AMD and Intel have smaller shares. Domestic AI training chips represented by Huawei's Ascend series have seen some shipments, but they lag NVIDIA in overall performance and ecosystem maturity. For example, Tencent-backed cloud product T20 delivers 32-bit single-precision performance of 32 TFLOPS, higher than A100's 19.5 TFLOPS and more power efficient, but its memory bandwidth is less than one third of the A100, leaving a gap for machine learning and deep learning workloads that require high bandwidth.

Huawei Ascend Leads Domestic Share

In October, imports of high-end AI chips such as NVIDIA A100, A800, H100, and H800 were further restricted, making domestic substitution imperative.

High-end AI chip exports restricted

Huawei ranks among the leading AI chip suppliers. Data show that in 2022 China shipped about 1.09 million AI accelerator cards in the open market, with NVIDIA holding 85% market share and Huawei about 10%, making Huawei the leading domestic supplier.

This year, after addressing foundry constraints, Huawei's AI chip development has entered a faster growth phase.

Focusing on Chips and Expanding Channel Partnerships

In recent years Huawei gradually phased out its Taishan-branded servers to focus on core compute products such as Kunpeng CPUs and Ascend GPUs, creating market space and building a partner ecosystem. Ascend system partners such as Huakun Zhenyu, Yangtze River Computing, Shenzhou Kuntai, and Xiangjiang Kunpeng are backed by local state capital, expanding Huawei's computing industry ecosystem.

Huawei AI Server Supply Chain Breakdown

Referencing CICC's DGX H100 AI server value breakdown and consolidating available data, the estimated high-value components in an Ascend-based server are AI chips (about 60%), NAND storage (about 10%), DRAM (about 9%), CPU (about 7%), and network cards (about 2%).

Huawei Atlas 800 training server core module composition and estimated cost shares

As mainstream Chinese vendors roll out large models, AI compute demand will continue to rise. Coupled with escalated US sanctions that could affect parts of NVIDIA's revenue, Huawei's Ascend series is positioned to become a mainstream choice for AI compute centers in the Chinese market.

Domestic Substitution and Market Opportunity

IDC and TrendForce predict about 250,000 AI server shipments in China in 2023, and conservatively estimate shipments will exceed 500,000 units in the next two years. Based on CICC's teardown of NVIDIA A100 systems, 500,000 systems would imply total component market value exceeding US$85 billion. Average domestic AI server prices are roughly 40% to 50% of NVIDIA A100 system servers, so over two years the Chinese market component value is expected to be US$34.0 billion to US$42.5 billion.

With Huawei AI accelerator cards holding about 10% domestic share in 2022 and under 10% in the first half of 2023, improvements in domestic foundry capacity since the second half of 2023 suggest potential market share gains. Under a 50% market share scenario, the potential market for Huawei GPU and CPU AI server chips over the next two years could exceed US$13.0 billion, and the related server ecosystem could total over US$20.0 billion.

In summary, domestic AI chip vendors led by Huawei still lag international leaders such as NVIDIA in overall performance and software ecosystem maturity. However, with tightening export controls prompting many firms to shift from international procurement to local sourcing or in-house development, conditions are increasingly favorable for domestic chip suppliers, and the potential for substitution in the Chinese market is significant.