ALLPCB

ALLPCB

Overview

Solid-state drives (SSD) offer faster read/write speeds, lower latency, and better shock resistance compared with mechanical hard drives (HDD). SSD shipment share in the global disk market has grown steadily and exceeded HDD shipments for the first time in 2020. Since the first SSD appeared, manufacturing processes and interface standards have evolved to achieve smaller form factors and higher transfer rates. In recent years, the China SSD industry has accelerated, and the China market has continued to expand.

Definition

An SSD is a storage device built from arrays of solid-state memory chips, consisting of a controller and memory modules. Its interfaces, functions, and usage patterns are compatible with traditional hard drives, and form factors are often similar. Compared with HDDs, SSDs provide higher read/write performance and improved reliability. SSDs are widely used in military, automotive, industrial control, video surveillance, networking, power systems, medical, aerospace, and navigation devices.

Classification

Common classification criteria for SSDs include:

- Application: enterprise SSDs and consumer SSDs. Enterprise SSDs target data centers and servers with high load; consumer SSDs target personal PCs and mobile devices.

- Interface: SATA, mSATA, PCIe, M.2, etc., selected based on application and performance requirements.

- Storage medium: flash-based SSDs and memory-based SSDs.

Characteristics

The China SSD market is characterized by expanding market size, ongoing technological innovation, intense competition, government support and partnerships that facilitate development, a progressively complete supply chain, diverse user profiles, and expanding application domains.

Business Models

Business models in the China SSD industry are primarily based on product manufacturing and sales. Models include manufacturer-brand partnerships, vertical integration, combined online and offline sales, product differentiation, and customized services.

- Manufacturer-brand partnerships: manufacturers focus on production while brand owners handle marketing, sales, and after-sales service.

- Vertical integration: some large firms control the supply chain from chip production to SSD assembly to reduce cost and improve quality.

- Online and offline sales: SSDs are sold via e-commerce platforms and physical retail, each channel offering different advantages.

- Customization: suppliers provide tailored SSD solutions for data centers, industrial control, and other specialized applications.

Competition

The China SSD industry is highly competitive and fast-developing, involving international vendors and local entrants. Price competition is intense, benefiting consumers but pressuring vendor margins. Local firms aim to catch up with international high-end technologies and to build brand recognition and trust. Some firms use vertical integration to strengthen competitiveness, and many are expanding into data center and industrial markets, supported by government policies that encourage domestic industry development.

User Profiles

SSD user groups in the China market are diverse: individual consumers, gamers, data center and enterprise users, industrial control and embedded systems, government and research institutions, and automotive electronics.

- Gamers: the demand for faster game load times makes SSDs a common choice for PCs and consoles.

- Data centers and enterprises: growth in big data, cloud computing, and AI increases demand for high-performance, reliable storage.

- Industrial control and embedded systems: requirements for high reliability and long lifetime make SSDs suitable for industrial applications.

- Automotive electronics: as vehicles become more connected and software-driven, on-board storage requires speed, stability, and durability.

Supply Chain Analysis

The SSD supply chain comprises upstream raw material suppliers, midstream SSD manufacturers, and downstream OEMs, brand owners, and end users. Upstream components include flash memory, controller chips, and PCBs, which undergo wafer fabrication, packaging, and testing before assembly. Midstream manufacturers perform assembly and testing to produce standard-compliant SSD products. Globally, midstream production is concentrated in South Korea, Taiwan, and the United States; China has made progress in some areas but still faces technology gaps. Downstream activities include OEM integration, white-label sales, and end-user deployment.

Challenges for industry development include technical R&D complexity, shortages of core components, high investment risk, and global economic and trade uncertainties. Investment opportunities may focus on new storage technologies and high-end controller design. Bargaining power varies across the chain; flash memory manufacturers typically hold stronger negotiating positions. Supply-demand balance and stability are influenced by production capacity, market demand, and raw material supply.

Upstream

Upstream is the foundation of the SSD supply chain and includes component suppliers and parts manufacturers. Key components are flash memory, controller chips, and other parts such as PCBs and enclosures. Flash memory determines SSD capacity and performance; controllers manage data read/write and transfer. As technology advances, upstream suppliers must deliver higher-performance and higher-capacity flash and controllers to meet market needs.

Cost structure is commonly divided into design, manufacturing, and packaging/testing. In the production process, design accounts for about 30% of total cost, manufacturing 40%, and packaging/testing 30%.

Midstream

Midstream consists of SSD manufacturers who assemble components into final SSD products. These manufacturers typically maintain R&D and production capabilities to improve performance and reduce costs.

Market supply has grown steadily in recent years and is expected to have further room for development. Globally, the SSD market exceeded USD 55 billion and is forecast to grow at an average compound annual growth rate (CAGR) of about 15%, potentially exceeding USD 125 billion by 2026. In 2021, global SSD controller shipments reached 408 million units, up 16.57% year-on-year. Consumer SSD controller shipments accounted for 83.86%, enterprise SSD controllers 12.41%, and industrial SSD controllers 3.73%.

Downstream

Downstream covers distribution channels and end consumers, including OEMs, brand owners, and end users.

User demand is mainly from enterprises and individuals. Enterprises prioritize reliability; individuals focus on cost-effectiveness and reputation. Enterprise SSDs and consumer SSDs address different pain points: enterprises seek high reliability, performance, and data security; consumers emphasize price-to-performance ratio and durability. Surveys indicate 78% of enterprise users cite reliability as the primary purchase driver, while 56% of personal users consider price-to-performance and reputation as top factors.

Demand drivers include rapidly increasing data storage needs, which are expected to continue rising and to drive SSD demand.

Market Size and Outlook

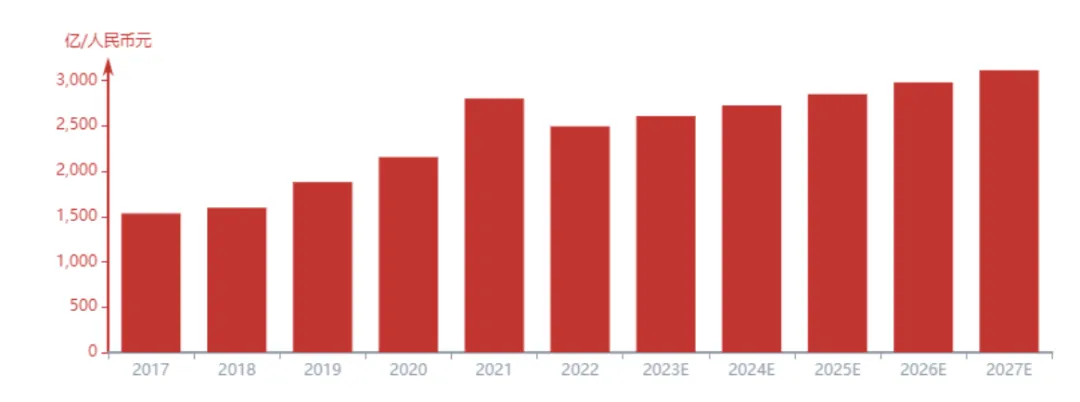

As a high-performance storage device, SSD has become mainstream. With continued growth in data volumes, market demand is expected to expand. In 2022, the China SSD market size was approximately CNY 249.4 billion. The China SSD industry is expected to maintain rapid growth, with the China market projected to reach CNY 311.17 billion by 2027.

In 2022, SSD revenue from enterprise customers grew by 25% year-on-year. SSDs remain an efficient and reliable solution for enterprise storage, with significant upside potential. The consumer market is also strong, as demand for high performance and improved user experience drives SSD adoption in personal computers, laptops, and gaming devices. In 2022, the China gaming market grew by more than 15%, supporting ongoing SSD demand for game content storage and load performance.

Competitive Landscape

The competitive landscape in the China SSD market is multi-polar. International giants such as Samsung, SK Hynix, and Western Digital hold significant positions. Domestic brands, including several well-known local firms, are also competing for market share.

Leading global vendors like Samsung, Intel, and Western Digital occupy the top tier. Over 95% of NAND flash used by local China SSD manufacturers comes from international suppliers such as Samsung, SK Hynix, Micron, Kioxia, and Western Digital. Samsung, Intel, and Western Digital together hold over 50% of the China SSD market, and these vendors offer vertically integrated design and manufacturing capabilities with industry-leading technology, investment, and revenue.

Below the top tier, there are emerging and local firms forming additional competitive tiers. These companies may be in rapid growth phases and gradually gaining market share. Second-tier firms include a few long-established local producers that are quickly narrowing the technology gap.

As new SSD technologies iterate and market demand diversifies, the competitive landscape may shift and intensify. Technological innovation, such as advances in 3D NAND, will accelerate competition by improving storage density and performance. For example, vendors producing higher layer-count 3D NAND have reported substantial performance gains. Meanwhile, diversified consumer demand across gaming, mobile workstations, and other segments will further shape market competition.